The Rise of Stablecoins and the Case for Coinbase

Stablecoins are becoming core financial infrastructure. Coinbase is built to capture the upside.

Coinbase is one of the cleanest public-market ways to underwrite stablecoin adoption.

The thesis is not simply that stablecoins grow. It is that Coinbase is structurally positioned to monetize that growth through USDC distribution, on-platform balances, Base, and its economic agreement with Circle.

If stablecoins become a major financial rail, Coinbase is not a passive beneficiary. It is one of the businesses most directly levered to the upside.

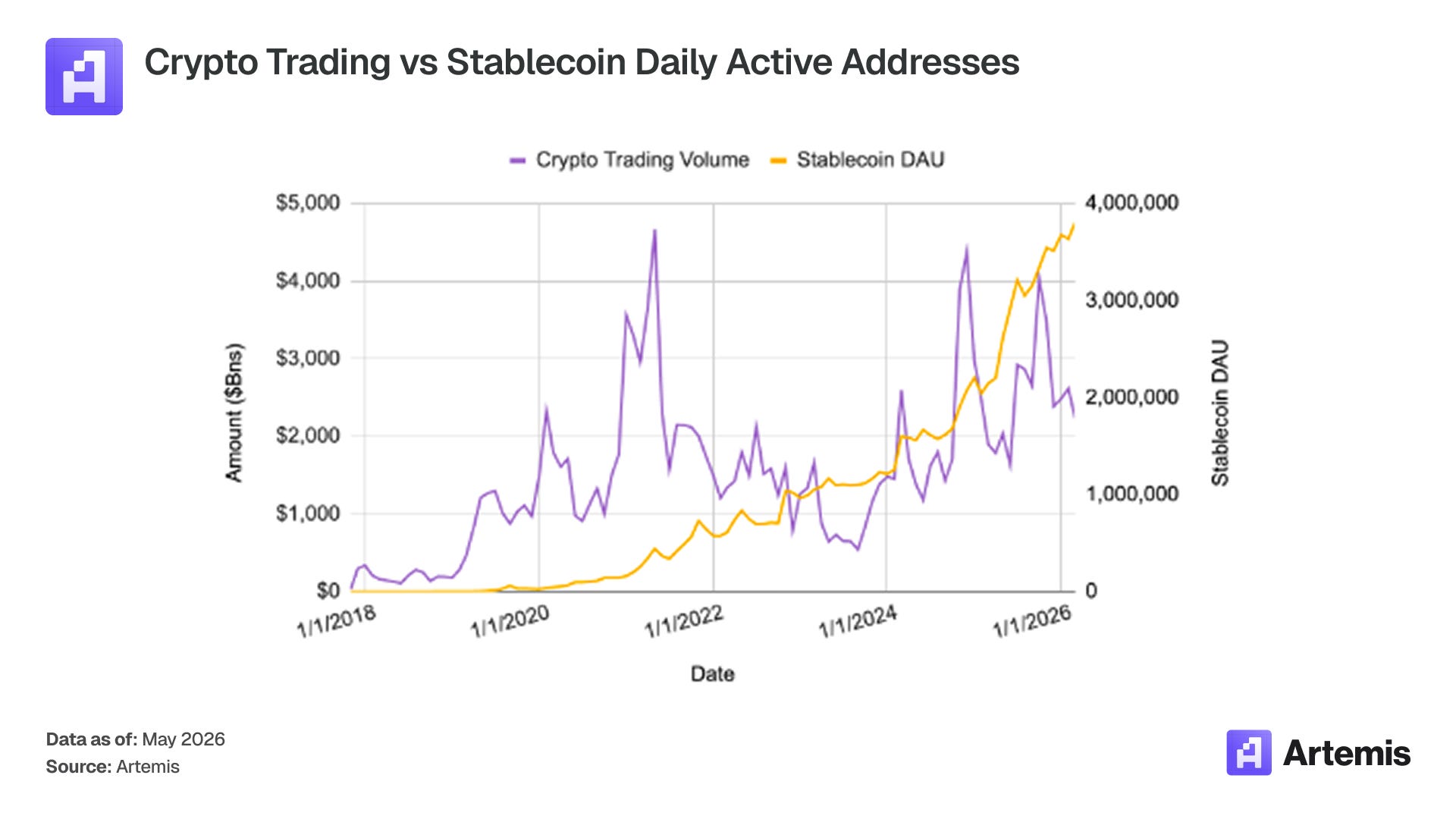

Stablecoins have become larger than crypto

Stablecoins used to be pseudonymous with crypto. As trading volumes and exchanges grew, the supply of stablecoins grew in parallel. But after 2021 we started to see something different. Usage metrics including transaction volume, daily active address and transactions continued to increase despite a downturn in crypto prices and trading. Stablecoins had “decoupled”, indicating broad based usage of all types of payments and store of value.

As more individuals adopted stablecoins, institutions followed. BlockRock launched a tokenized money market product, Circle had an IPO and regulation like GENIUS passed in the US. These developments turned many optimistic about the use of stablecoins, given their upgraded features to the traditional financial system. Even the US Treasury Secretary Bessent believes stablecoins could reach $3T by 2030, up almost 10x from today.

Coinbase is a clear beneficiary of the stablecoin mega-trend.

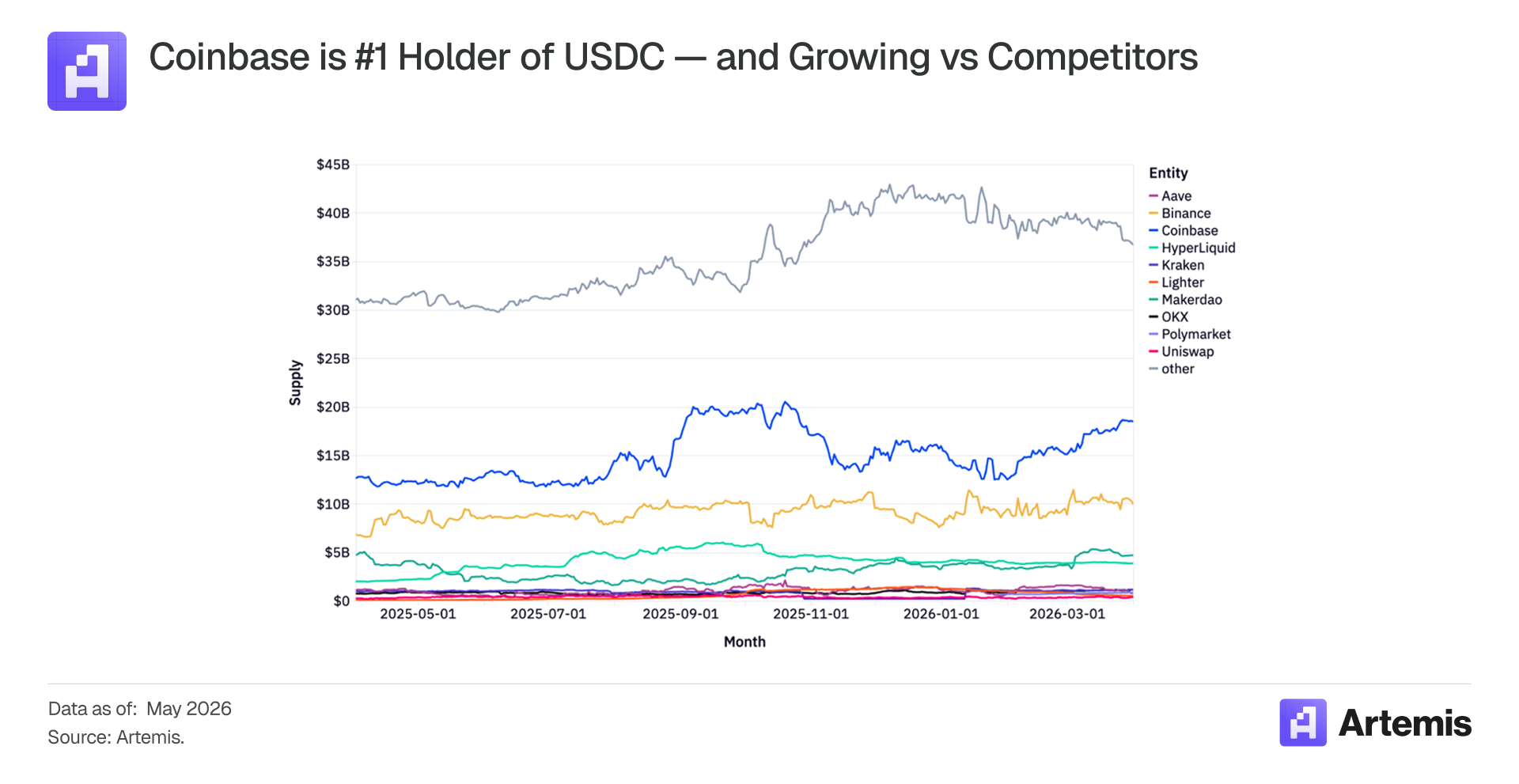

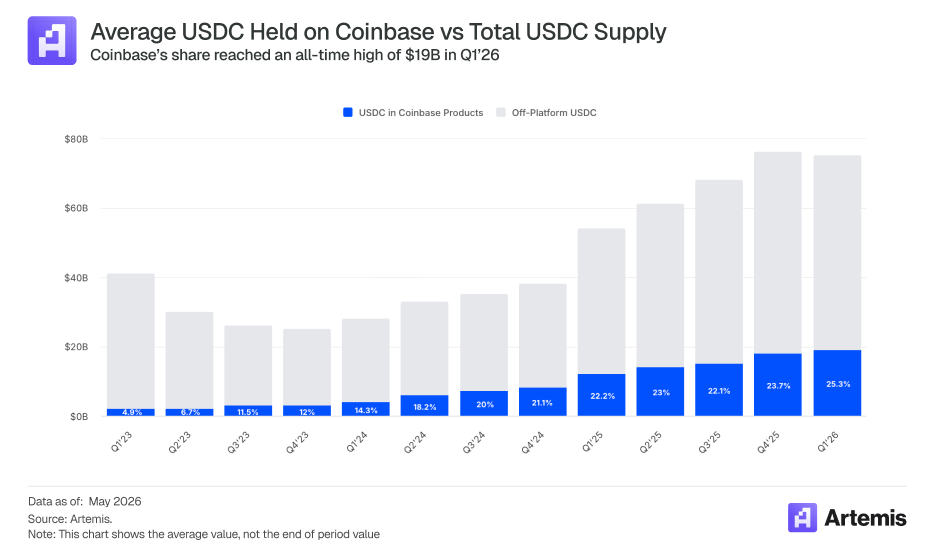

First, on-chain data tells a compelling story. Coinbase is the #1 holder of USDC on platform and is growing its lead over competitors. USDC on Coinbase is nearing an all time high as USDC is also hitting an all time high.

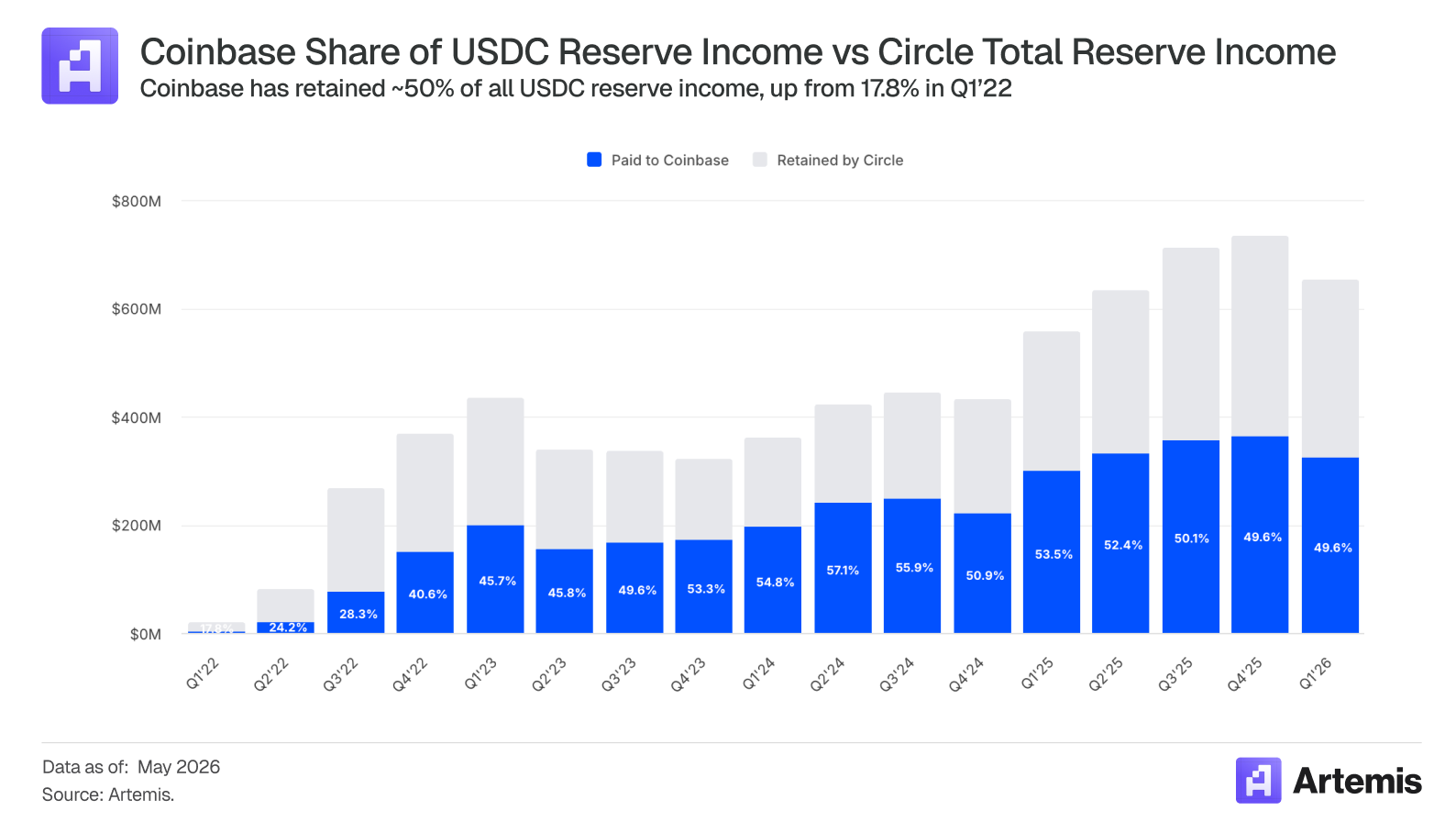

Second, we believe the USDC distribution agreement is Coinbase’s asset, not Circle’s. Circle’s share-of-revenue paid to Coinbase has climbed from 17.8% in Q1’22 to roughly 50% in each of the last two years.

The structural reason is straightforward: Coinbase earns roughly 100% of the yield on USDC held in its products and a 50% share of off-platform balances under the Payment Base waterfall. As Coinbase’s distribution grew (Q1’26 average USDC held in Coinbase products hit $19B, an all-time high), its waterfall share grew with it.

From an investor’s standpoint, Coinbase effectively gets issuer-like economics without the cost or overhead of being an issuer. The Collaboration Agreement runs in 3-year terms and auto-renews provided that three thresholds are met (Product, Company, and Reseller). Public filings indicate that, if those thresholds are satisfied, “the Circle Agreement cannot be terminated.” The renewal mechanism is not a renegotiation cliff, rather a continuation lock. As Coinbase is in full control of the renewal terms, this could be viewed as a perpetual agreement. For Coinbase, the upside scenarios (regulatory clarity drives stablecoin payments to scale, USDC market cap expands meaningfully) flow directly through the same contractual share. The contract is structured to compound Coinbase’s position regardless of who runs Circle.

Third, clear regulation is coming into play. The CLARITY Act’s relevance to Coinbase’s stablecoin economics is also greater than is widely appreciated. Coinbase’s distribution and reserve-share arrangements with Circle generate a revenue stream that, on current rate assumptions, rivals the issuer-level economics earned by Circle itself, and Coinbase’s USDC rewards program contributes a further line whose ultimate scale depends on how the Tillis-Alsobrooks compromise is finally drafted. The market underweights the magnitude and durability of these stablecoin-linked revenue lines and treats them as adjuncts to the exchange business rather than as core infrastructure economics in their own right. The CLARITY Act, by formalizing the broader regulatory architecture in which stablecoins clear, settle, and circulate — and by clarifying the registered intermediaries through which institutional stablecoin flows transit — strengthens that argument. It reframes Coinbase’s stablecoin franchise as the application layer of a regulated and rapidly institutionalizing system, rather than as a discrete consumer product line whose value rises and falls with retail token trading volumes.

Future Growth of USDC

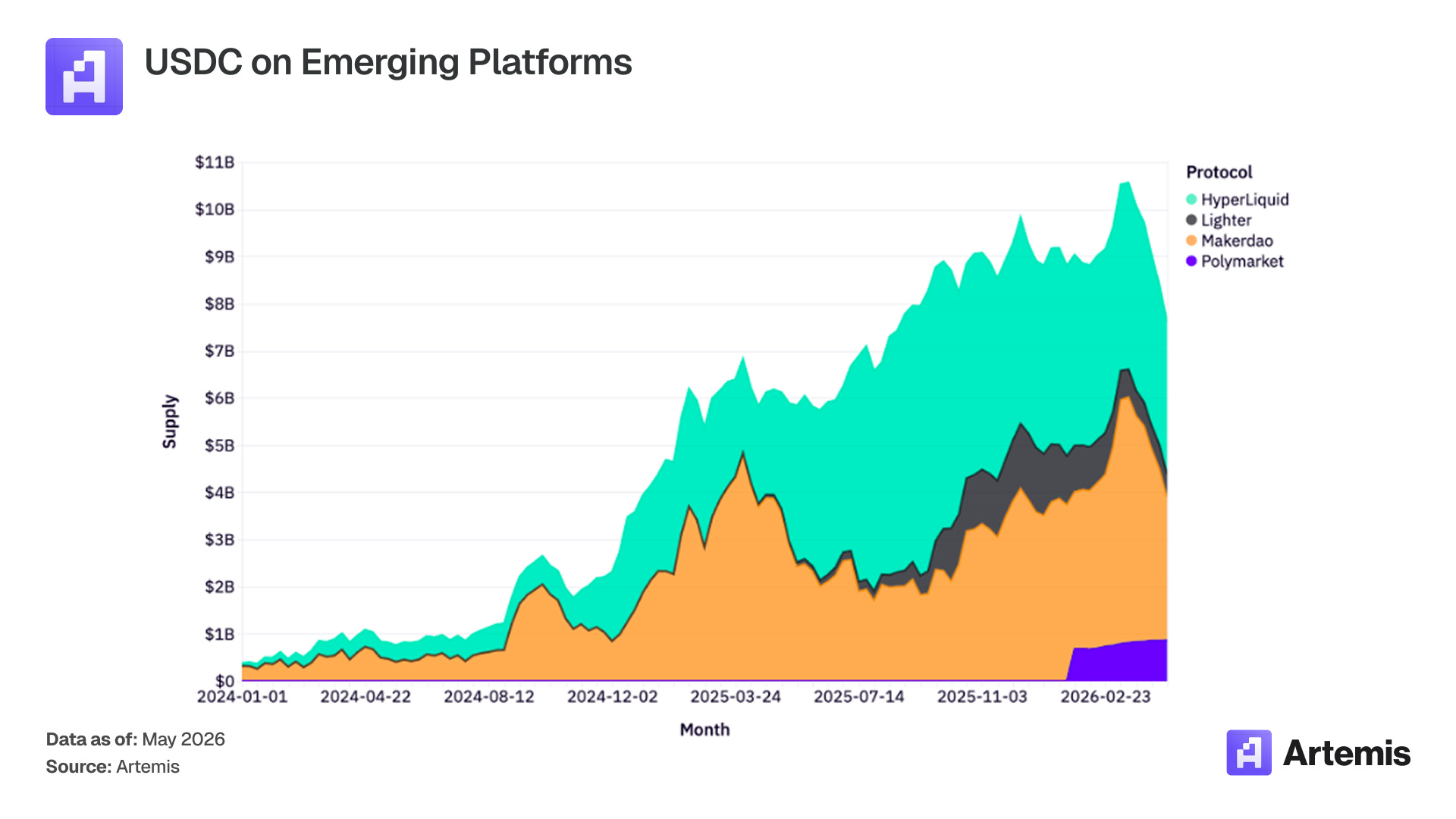

As blockchain rails support increasingly interesting applications, USDC has been often used as the settlement or collateral asset integral to those applications. We’ve seen drastic growth in USDC supply in protocols like Polymarket, Hyperliquid, MakerDAO, etc. As new financial use cases emerge on blockchain platforms, USDC will continue to compound its position as core infrastructure.

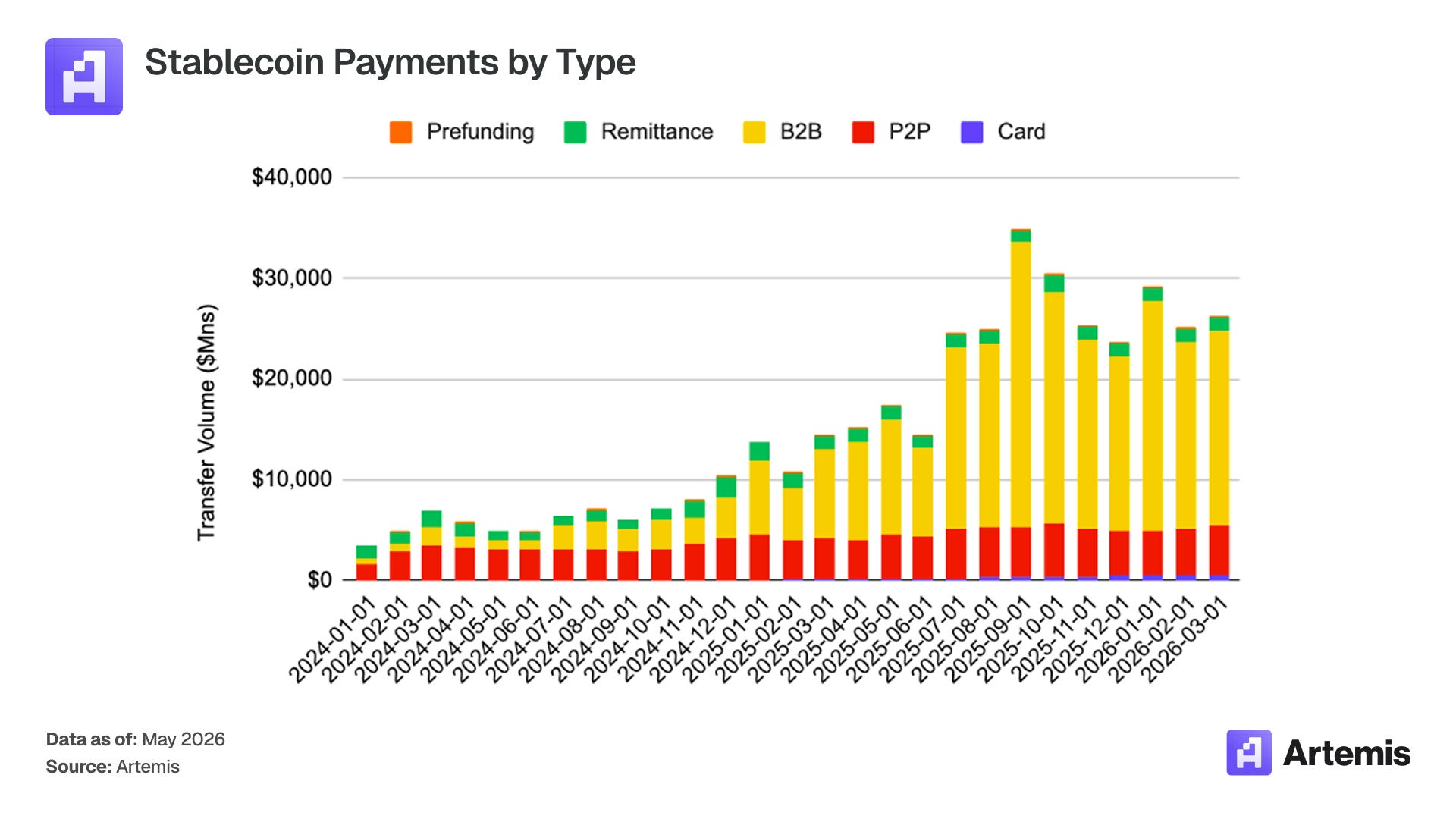

We believe Coinbase is in a good position to capture the next wave of stablecoin use cases: payments. Payment types on card rails (B2B, B2C) have all increased significantly over the past year, and USDC has been gaining share in these types of transactions.

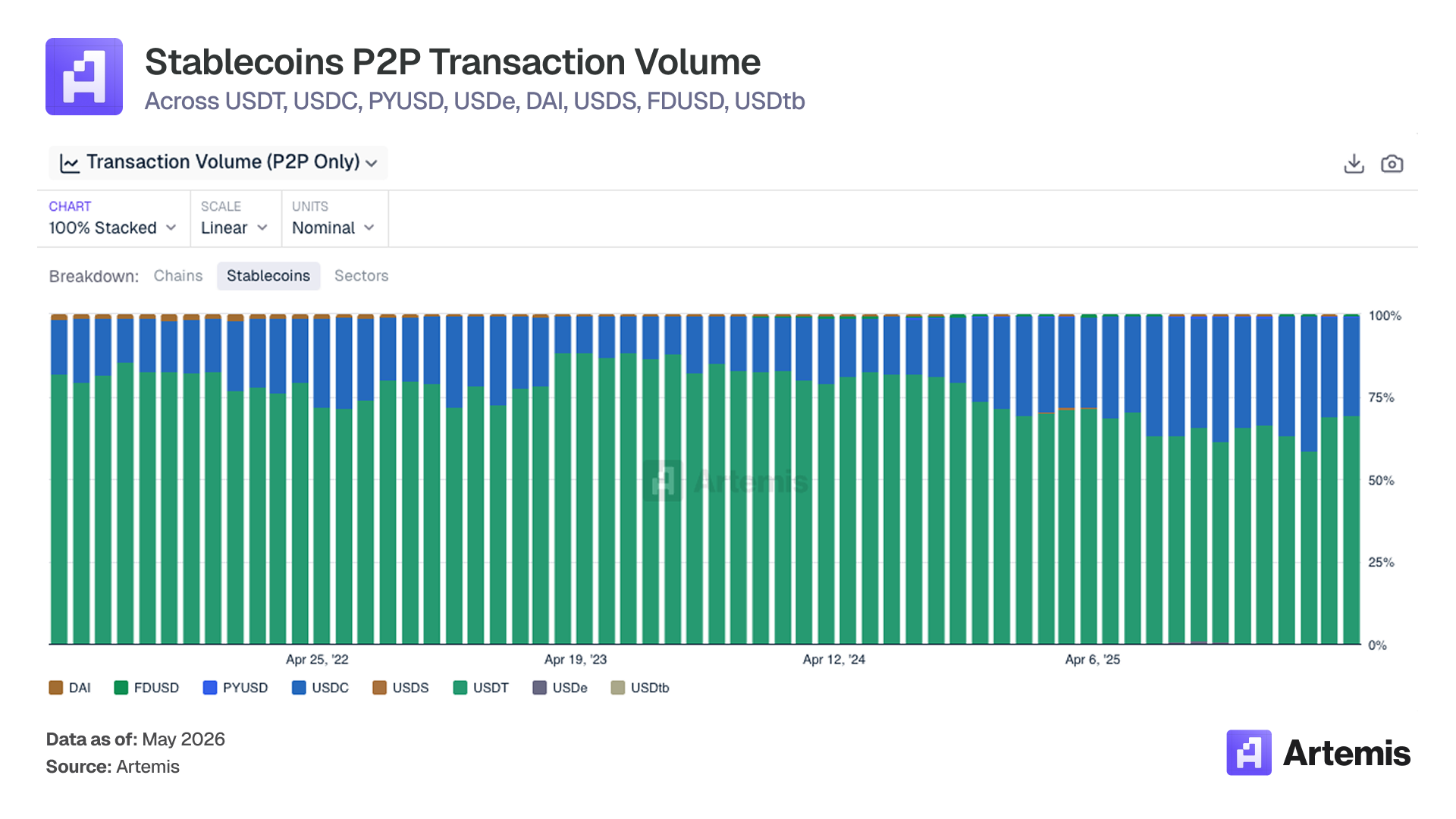

When looking at address to address transfers of USDC, a proxy for these types of transactions, we can see USDC gaining share against USDT.

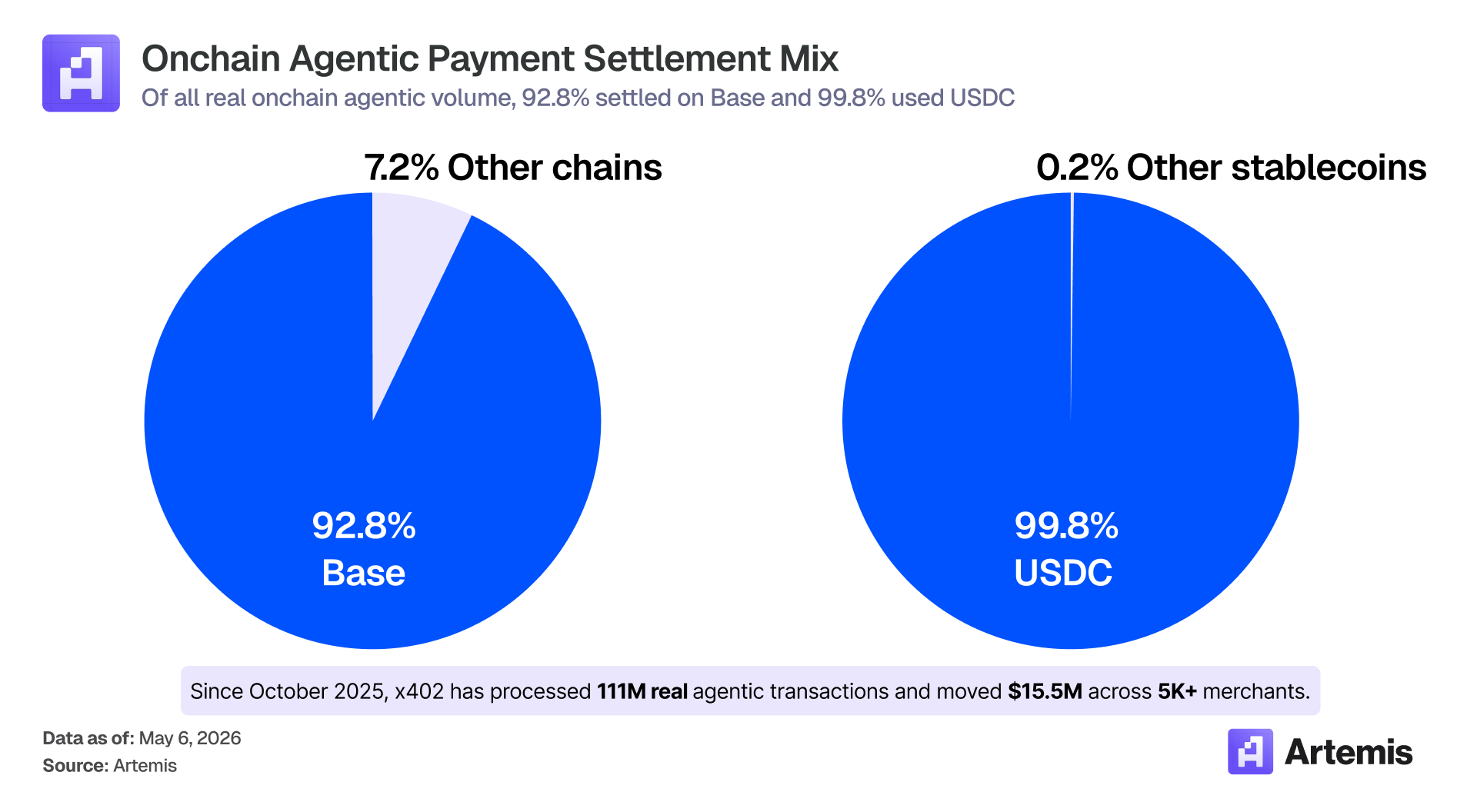

Most investors think Stripe ($159B as of Feb ‘26) and Tempo are the clear winner of agentic commerce but a look at onchain metrics shows otherwise: 92.8% of real agentic payments volume happens on Base, while 99.8% are settled in USDC.

For a deeper look at how agentic commerce could create the next major source of stablecoin demand, read our full agentic Coinbase thesis here.

Conclusion

Coinbase has already proven to be the leader in USDC and USDC economics. As stablecoins continue to grow and see new use cases in trading and commerce, we believe Coinbase is well positioned to capitalize on all of these trends. As new entrants enter the space and regulation becomes clear, we believe there is a path for stablecoins to reach 3 trillion and for Coinbase to have a meaningful share of that on platform.

Disclosure: This material is provided for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other form of advice. The views expressed are those of the authors and should not be relied upon as a recommendation to buy, sell, or hold any asset. The authors or affiliated entities may hold positions in the assets discussed. You should conduct your own research and consult appropriate financial professionals before making any investment decisions