The Shape of a Market: The Case for Kraken

The Setup

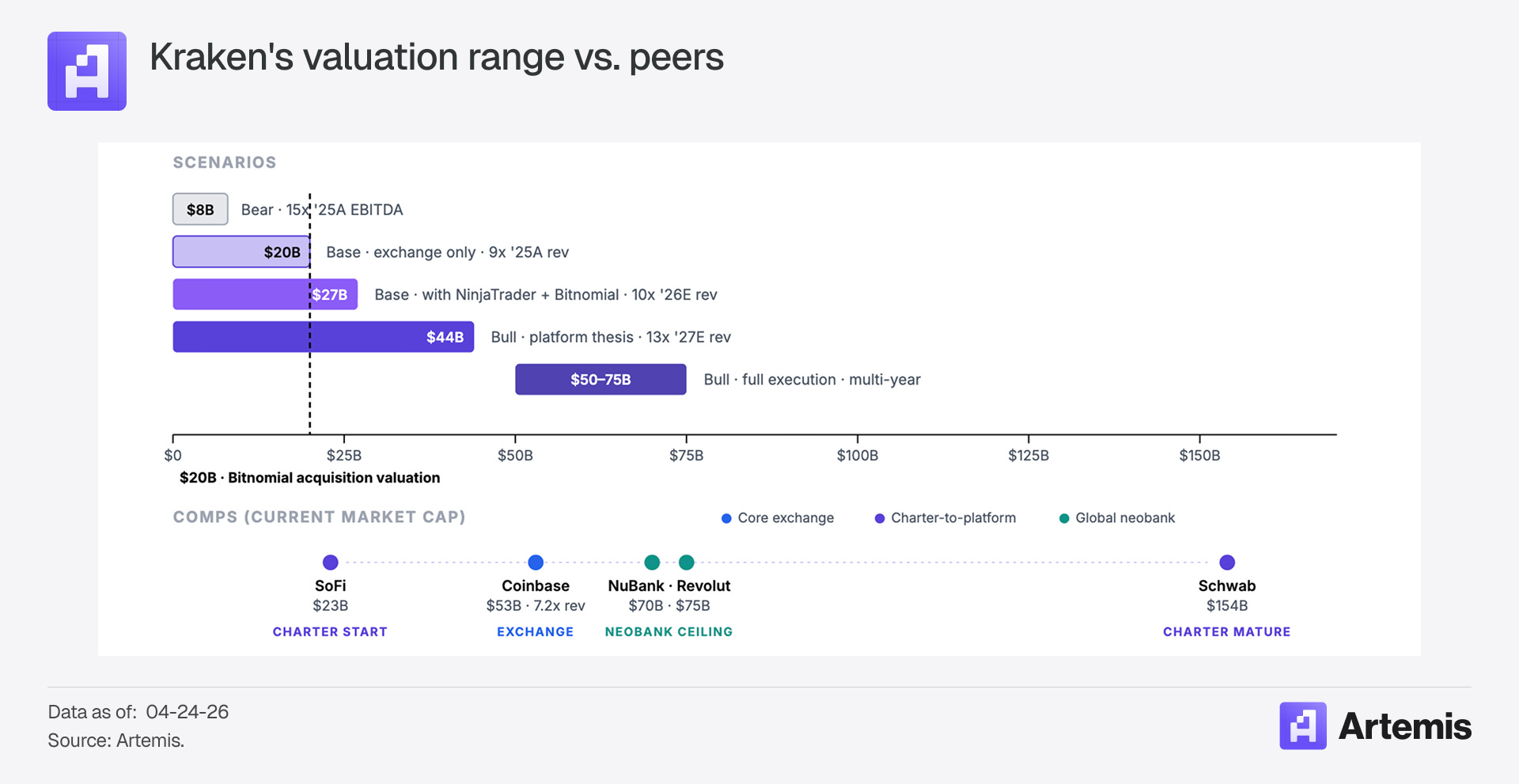

Shortly after raising $800M from the likes of Jane Street, Citadel Securities, valuing the firm at $20B, Payward (Kraken’s parent company) confidentially filed an S-1 with the SEC signaling its intent to go public. This would make Payward the second publicly traded crypto exchange after Coinbase. 4 months later, in March 2026, they froze their IPO plans citing difficult market conditions.

A first pass would read this as a failed and shelved IPO. But in the five months since the filing, Kraken has accelerated momentum by:

Becoming the first digital asset company with a Master Account at the Federal Reserve

Closing its acquisition of Backed Finance, vertically integrating issuance for tokenized equities

Announcing its partnership with Nasdaq to build a gateway for tokenized assets

Closing its $550M acquisition of Bitnomial, and obtaining the full set of CFTC licenses

Announcing that Deutsche Boerse acquired a $200M secondary stake

That is a lot of activity for a business the market views as simply a crypto exchange. The $20B was reaffirmed in April 2026 by the Bitnomial transaction, per Payward’s press release (Payward). This piece argues that at $20B, the payoff distribution is asymmetric: downside bounded by the crypto-exchange floor, upside open-ended on execution of the clearing, tokenization, and charter stack.

The Business Today

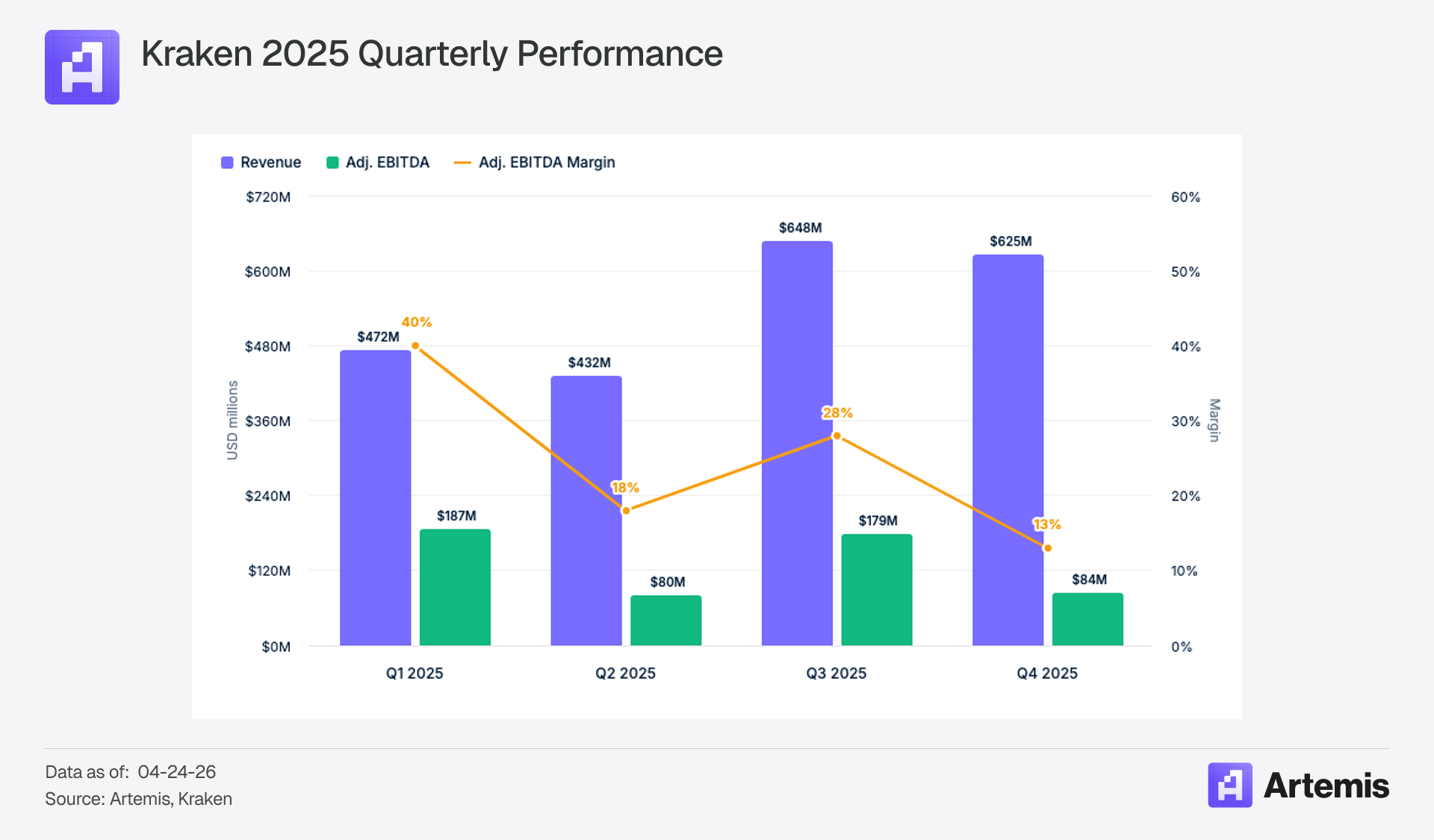

In 2025, Kraken generated $2.2B in adjusted revenue (+33% YoY), with $531M in adjusted EBITDA. On the operational side they ended the year with 5.7M funded accounts (+50% YoY), $48B in assets on platform (+11% YoY), and $2T in platform transaction volume (+34% YoY). Kraken’s revenue mix is more diversified than most would assume: 47% trading, 53% asset-based (custody, yield, payments, financing). On any given day, the majority of Kraken’s revenue does not come from trading. (Kraken Financials)

The Upside Levers

The Regulatory Stack

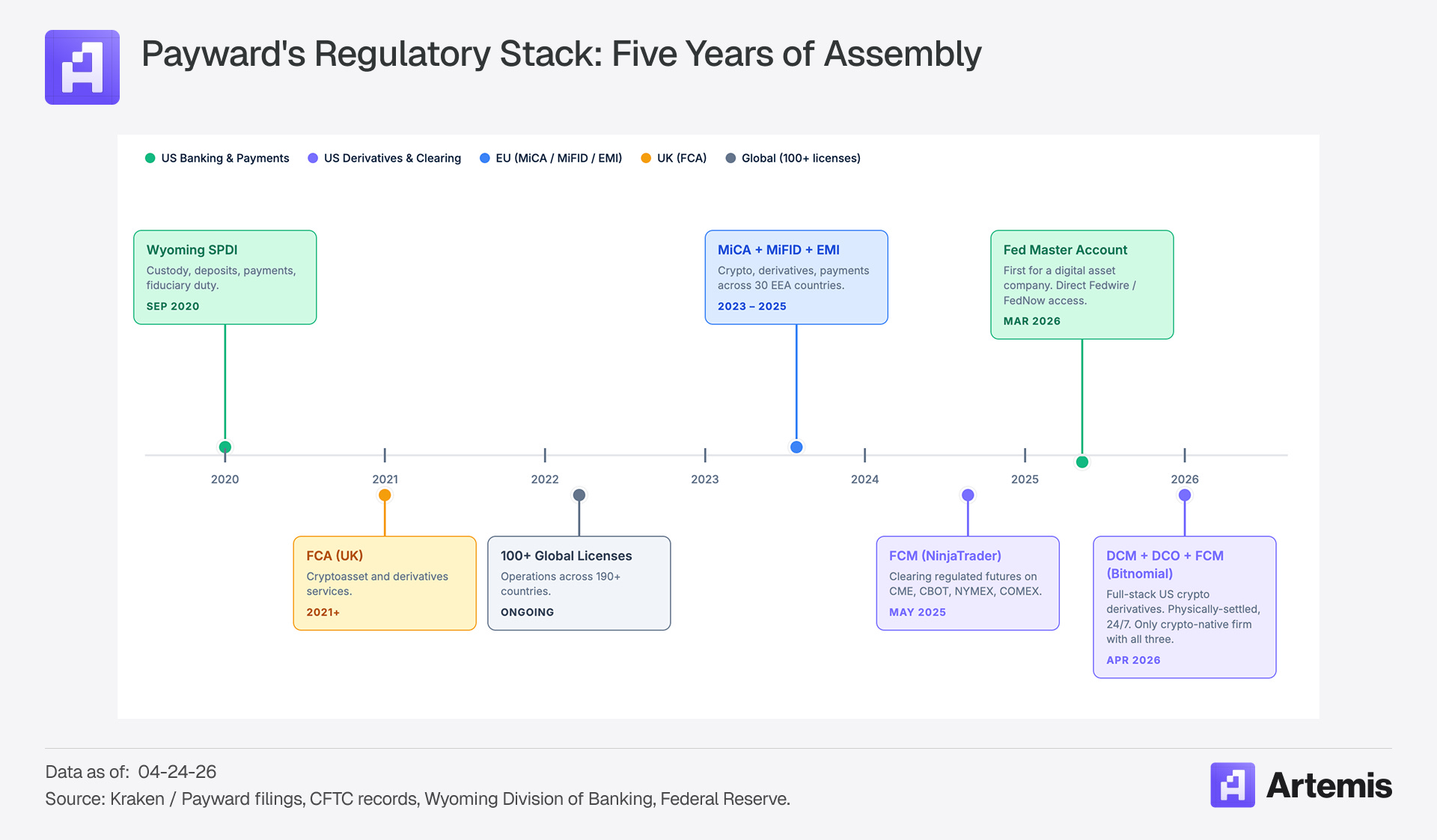

Kraken has spent over five years and billions of dollars assembling a regulatory and infrastructure stack that is unique in the crypto industry.

The Bitnomial acquisition is highly significant as it gives Kraken all three CFTC licenses required for a full-stack domestic crypto derivatives business. Designated Contract Market (DCM) is the exchange license, Derivatives Clearing Organization (DCO) is the clearinghouse, and Futures Commission Merchant (FCM) is the brokerage.

“The shape of a market is determined by its clearing infrastructure, not its front end. The US has had no clearing infrastructure built for digital assets. Bitnomial spent a decade building it: crypto settlement, crypto collateral, continuous 24/7 markets. These are capabilities that cannot be retrofitted onto legacy systems.” — Arjun Sethi, Co-CEO

Coupled with the NinjaTrader acquisition which gave them retail futures distribution to 2M users, this gives Kraken a vertically integrated derivatives stack from UI to clearing. Being first to combine DCM, DCO, and FCM with physically-settled, crypto-native collateral and 24/7 markets under one roof matters. Clearinghouses are natural monopoly businesses with strong economies of scale. Once institutional firms connect to Kraken’s DCO and build their risk systems around it, switching costs are significant. CME didn’t dominate futures because it had the prettiest front end, it dominated because everyone cleared there.

The broader crypto industry is converging on regulated infrastructure through different paths. Coinbase recently received conditional approval for an OCC national trust charter, which provides federal uniformity for custody and settlement across all 50 states — a natural fit for a company that custodies assets for most US spot crypto ETFs. Kraken’s Wyoming SPDI is a state-level charter but with broader functional powers: it can accept deposits, offer payment services, and operate under fiduciary duty. That distinction matters because it allows Kraken’s roadmap to extend into banking products (deposit accounts, stablecoin issuance, FedNow-powered payments) that a custody-only charter would not support. The Fed Master Account, secured in March 2026, is the infrastructure layer that activates those capabilities.

Tokenization and xStocks

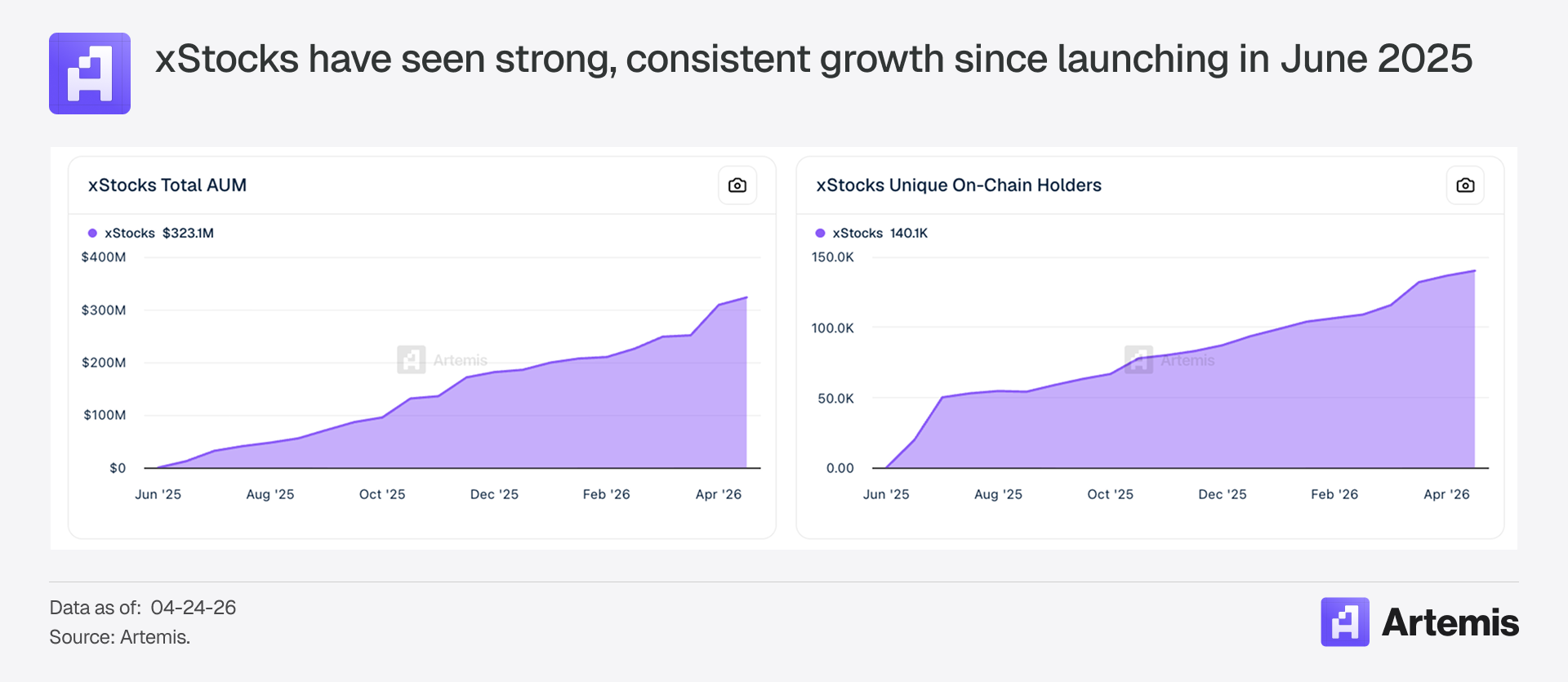

Kraken launched xStocks in partnership with Backed Finance in June 2025, enabling 24/5 trading of tokenized US stocks and ETFs. In less than a year, the product has grown to +$320M in AUM, and 100+ tokenized stocks across Ethereum, Solana, Ink and Ton. xStocks is the largest tokenized stocks product in the world today.

In December 2025, Kraken announced its acquisition of Backed Finance, the Swiss issuer that mints the tokens. Kraken now owns the full vertical: issuance (Backed), trading (Kraken), settlement (Ink) and custody.

This momentum compounded with announcement of the Nasdaq partnership:

“Nasdaq’s partnership with Payward... will be focused on designing an equities transformation gateway to enable issuers and investors to move seamlessly between permissioned and permissionless environments.” (Nasdaq)

Kraken is becoming the owner of the critical infrastructure that connects legacy securities with public blockchains. Nasdaq’s Equity Token framework is expected operational H1 2027, with Payward as the primary settlement layer. (Nasdaq has partnered on tokenization before, including with Ondo and Republic. Commercial terms are undisclosed, and the product is not yet live.)

Coinbase and Robinhood have announced tokenized stock ambitions, but as of April 2026 neither has shipped a backed product. Kraken’s xStocks already have $323M in AUM, 140K on-chain holders, and DeFi composability across multiple protocols. Kraken has a first-mover position, but at $320M AUM it’s better understood as option value than as a moat. The Nasdaq partnership is the catalyst that could convert that option into something durable.

Ink: The Toll Booth

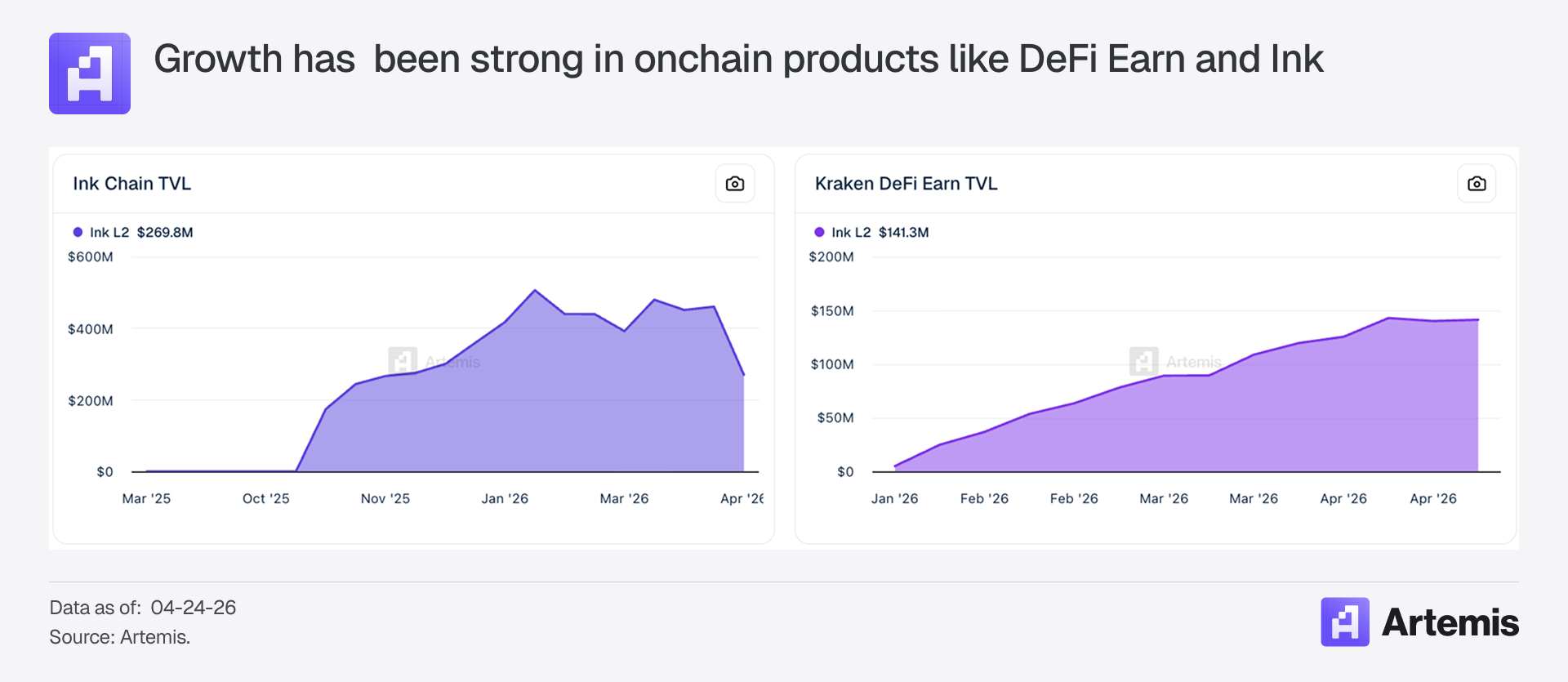

Ink is Kraken’s Ethereum L2 on the OP Stack. Mainnet launched December 2024; TVL is around $270M (after the KelpDAO exploit). App revenue grew from $500K in October 2025 to $5.77M in January 2026. Kraken runs the only sequencer, meaning 100% of gas fees flow to Kraken.

If xStocks settlement migrates fully to Ink, every tokenized equity transfer, DeFi interaction, and lending transaction will generate fees for Kraken’s sequencer. It functions as a toll booth between traditional finance and on-chain markets. Ink is early relative to more established L2s like Coinbase’s Base which generated roughly $75M in sequencer revenue in 2025, making it the largest L2 by that metric. But Ink’s trajectory is steep and it has a differentiated asset (xStocks) to drive activity that other L2s lack.

The Platform Vision

Management has been explicit about the growth vectors: expanding asset classes (”Tokenized equities, FX, futures, and real-world assets extend that same infrastructure…”), asset productivity (”Custody, payments, yield, financing, and settlement activity…”), and global expansion via a “single global core” supporting localized onramps (Kraken).

Asset productivity matters most for valuation. The pattern is familiar: Schwab’s 2003 bank charter was widely questioned for a discount broker; NII eventually became its largest revenue source. The analogy has limits, though. When Schwab got its charter it was already the largest US discount broker with $800B in client assets. Kraken has $48B on platform and a brand-new Fed account. The better near-term comp is SoFi: NII grew from $252M (2021) to $2.2B (2025), yet SoFi trades at ~$23B. The market credits banking economics but does not hand out a growth premium. Kraken’s differentiation has to come from the crypto-native angle.

The early evidence is there. Instant USD withdrawals (24/7/365, 1.5% fee, $50 cap) likely run on FedNow. Krak App has 450K+ downloads across 130 countries (The Block). The Unified Wallet already cross-margins spot, margin, and futures within crypto. The logical next step, unified margin across crypto + xStocks + NinjaTrader futures, would be a highly differentiated product, and Kraken’s license stack is uniquely suited to build it.

The Stablecoin Gap

Stablecoins remain Kraken’s most significant competitive gap. Coinbase’s USDC revenue-sharing arrangement generated an estimated $1.35B in 2025, high-margin and recurring. Kraken has no equivalent. USDG (a consortium stablecoin with Robinhood, Paxos, Galaxy) has a $1.95B market cap versus USDC’s ~$76B. Kraken also has a distribution partnership with Circle and plans to issue its own MiCA-compliant stablecoin via Ireland. Closing this gap, whether through USDG scale, a US stablecoin under the SPDI post-GENIUS Act, or some other mechanism, is a key strategic question.

Valuation

Kraken does not fit one bucket. It spans crypto exchange, futures clearing, tokenized securities, banking, and L2 infrastructure.

At $20B, Kraken is priced roughly fairly for what the market can verify today: a cyclical exchange at 8-9x revenue with a maturing derivatives stack. Sophisticated investors, including those in the November 2025 round, priced in what they could see. What’s less priced is the distribution of outcomes from here. The downside is anchored by the exchange floor: base case implied EV sits in the $20-27B range even if the platform thesis never materializes. The upside depends on execution across three independently live but unproven catalysts: Bitnomial clearing scale, xStocks in the US, and banking products on the Fed master account. A bet here is not a bet that the market is wrong about today’s Kraken. It’s a bet that the distribution of outcomes from $20B is asymmetric, with bounded downside and open-ended upside on execution.

Risks

Crypto cyclicality is the biggest near term risk. Revenue swung from $696M (2023) to $2.2B (2025). Staking, margin interest, and custody fees all correlate with crypto prices. No matter how you slice the 47/53 mix, Kraken’s revenue is crypto-beta.

US xStocks approval is the biggest catalyst and biggest uncertainty. Without the US, xStocks is meaningful, but not thesis-changing.

The regulatory moat erodes over time. As crypto regulation clarifies, more companies acquire more licenses. Kraken’s advantage is the combination and head start, not permanence.

The institutions will come. If tokenized equities will proliferate meaningfully as we believe, BlackRock, JPMorgan, Fidelity, and Goldman will enter with larger balance sheets, deeper relationships, and existing distribution.

What could go right

US xStocks launch: step function in volume, users, and narrative

Banking products on Fed master account: recurring, non-cyclical revenue

Cross-margin product: attracts institutional capital without a current home

Bitnomial clearing infrastructure: enables physically-settled crypto derivatives at scale

Stablecoin issuance under SPDI charter: direct NII stream

NinjaTrader cross-sell: 10% conversion of 2M futures traders = 200K high-value accounts

Kraken is the first crypto-native firm to assemble the full US clearing stack and holds the largest tokenized-equities product globally. Whether that advantage compounds or gets competed away will define whether this is a $20 billion exchange or something considerably larger. No other company has clearing, tokenized equities, a bank charter, and a Fed master account under one roof. Any single piece is replicable. The combination, assembled first, is what makes the bet.