This Week in Digital Finance (07.10.2026)

Robinhood launches its own L2 for 24/7 tokenized stocks, a 140-partner consortium unveils Open USD, and Kalshi clears $33B in a single month as the "boring-names" rotation carries the Dow past 53,000.

Market Overview

Global risk assets closed the first full week of July on firm footing, but beneath a placid index tape the composition of leadership shifted hard. The Dow crossed 53,000 for the first time and set new record closes, capping a first half in which the Dow rose ~8.9%, the S&P 500 ~9.6%, the Nasdaq ~12.8%, and the Russell 2000 ~22% – its best first half since 1991. The macro backdrop turned friendlier: a soft June jobs report and new Fed Chair Kevin Warsh’s comment that inflation risks had come down revived hopes of a less-hawkish Fed, reversing months of “higher-for-longer” repricing. The counterweight was geopolitics: fresh attacks in the Strait of Hormuz and the revocation of Iranian sanction waivers pushed oil and the 30-year Treasury yield higher (back above 5%), lifting the discount-rate hurdle for long-duration growth just as Q2 earnings season opened. By later in the week that tension produced a genuine chip rout: Samsung’s record quarterly guidance on July 7 could not stop a semiconductor sell-off, and the Nasdaq wobbled even as the broader tape held.

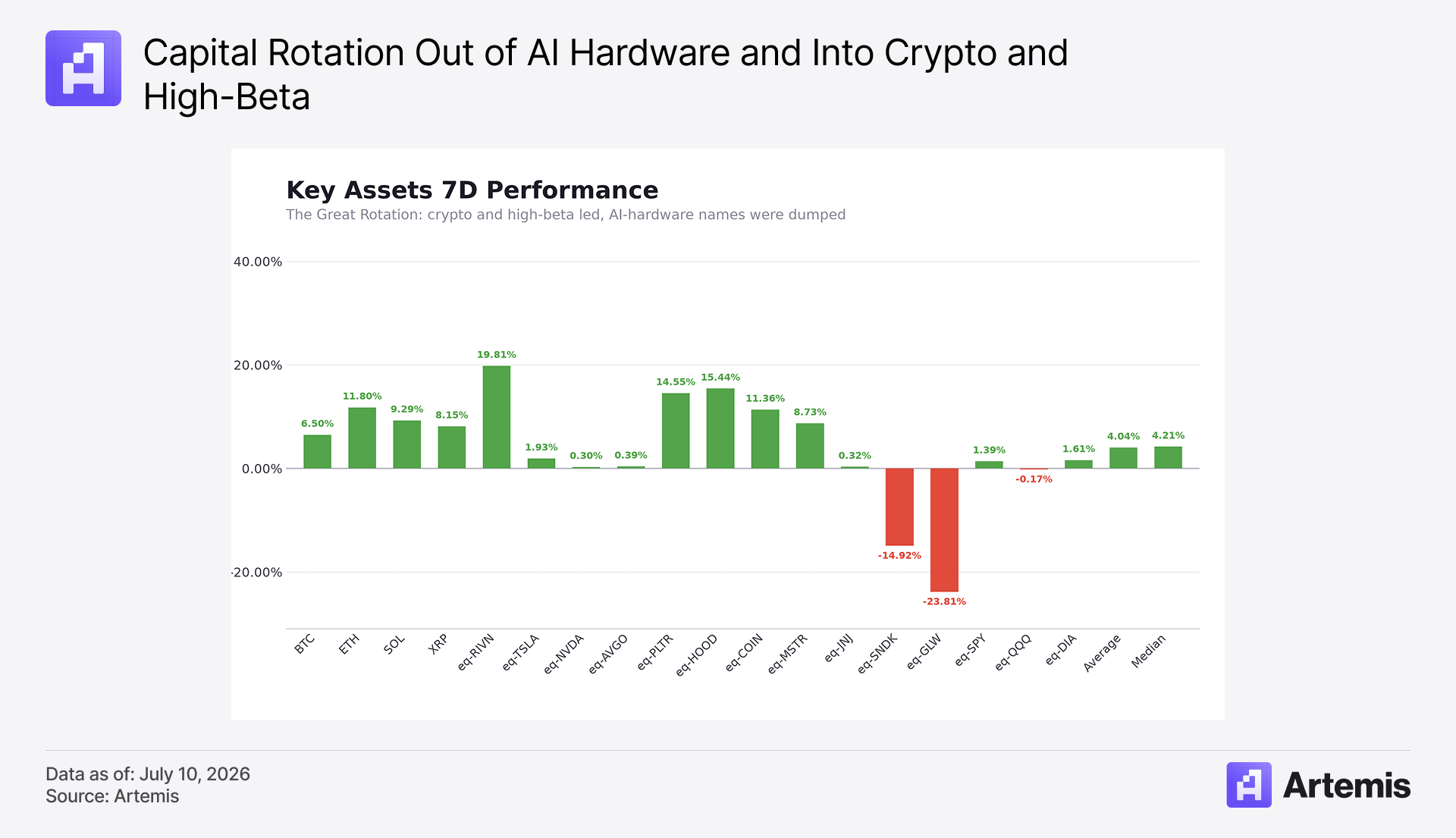

The week’s scoreboard tells the rotation story in one picture. The biggest single-name winners were not the AI-hardware leaders but recovering high-beta and crypto-levered names: Rivian (+19.8%), Robinhood (+15.4%, riding its Robinhood Chain launch), Palantir (+14.6%), Coinbase (+11.4%) and Strategy (+8.7%), alongside a sharp crypto bounce (ETH +11.8%, BTC +6.5%). The benchmarks advanced only modestly (Dow +1.6%, S&P 500 +1.4%, Nasdaq-100 −0.2%). The damage was concentrated in the AI-capex complex: Corning (−23.8%) and SanDisk (−14.9%) were dumped even as the mega-cap AI names (NVDA +0.3%, AVGO +0.4%) went sideways — a textbook “sell the crowded winners, rotate into everything else” week.

Today We Highlight:

The Great Rotation: Capex-payoff doubts pull money out of AI hardware and into "boring" value.

Robinhood Chain: Robinhood ships its own Arbitrum-based L2 with 24/7 tokenized stocks and a day-one DeFi stack.

Open USD: A ~140-partner consortium (Google, Visa, Stripe, BlackRock, Coinbase…) unveils a stablecoin for “global money movement.”

The Great Rotation: AI Collapses as “Boring” Stocks Rise

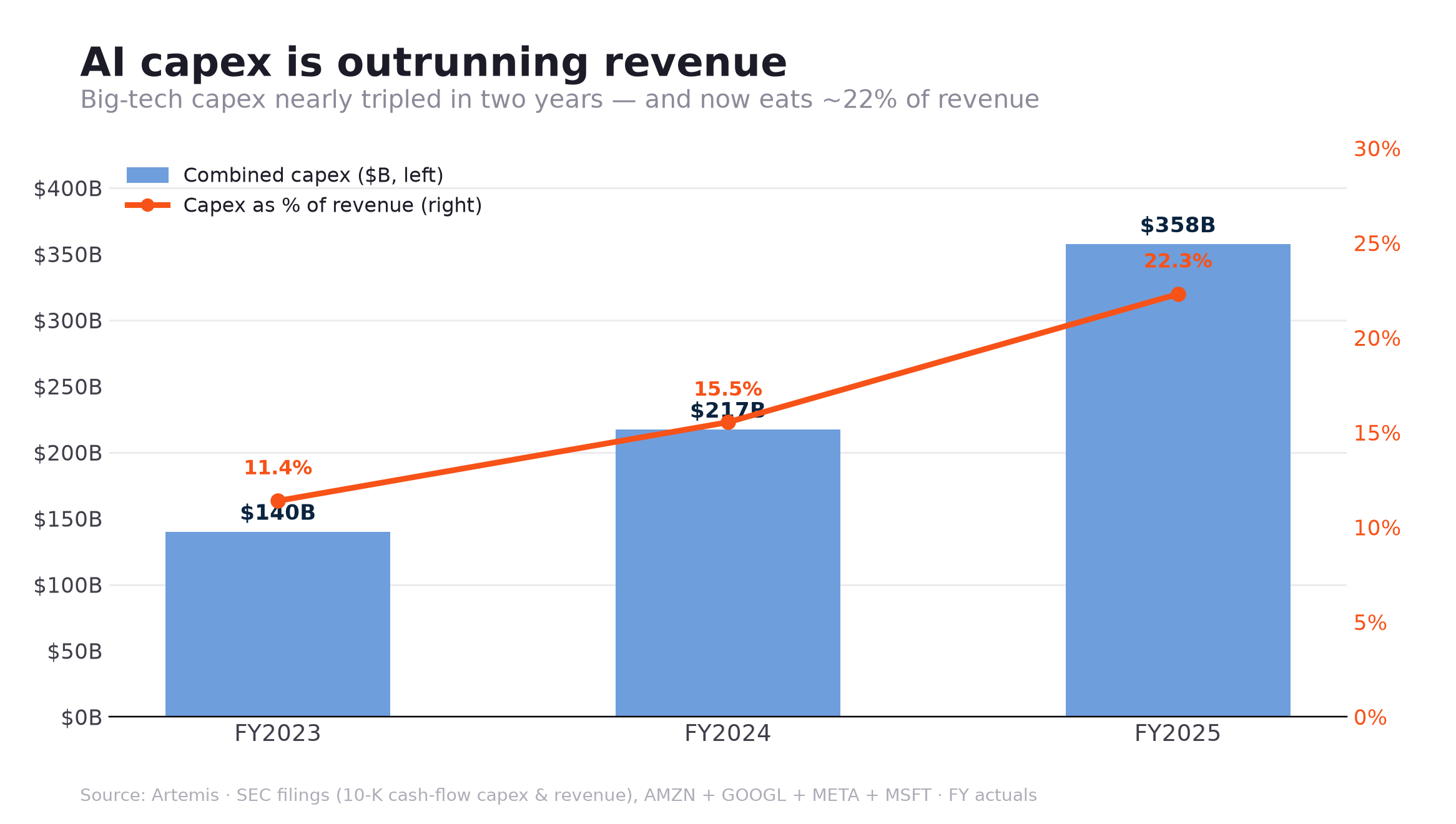

The most important market story of the week is that capital is rotating out AI hardware and into the value and defensive names that sat out the 2025 boom. The proximate cause is a growing investor demand for evidence that record AI capital spending will actually pay off. Big-tech AI capex is set to climb another ~50% in 2026 to well over $600bn, and the gap between investment and revenue is now wider than the 2001 telecom bubble as capex is growing roughly 46% faster than sales. With US tech/AI multiples near EV/EBITDA of ~25x, the market has begun to punish spending even when operational results beat, because the fear is margin compression as monetization lags.

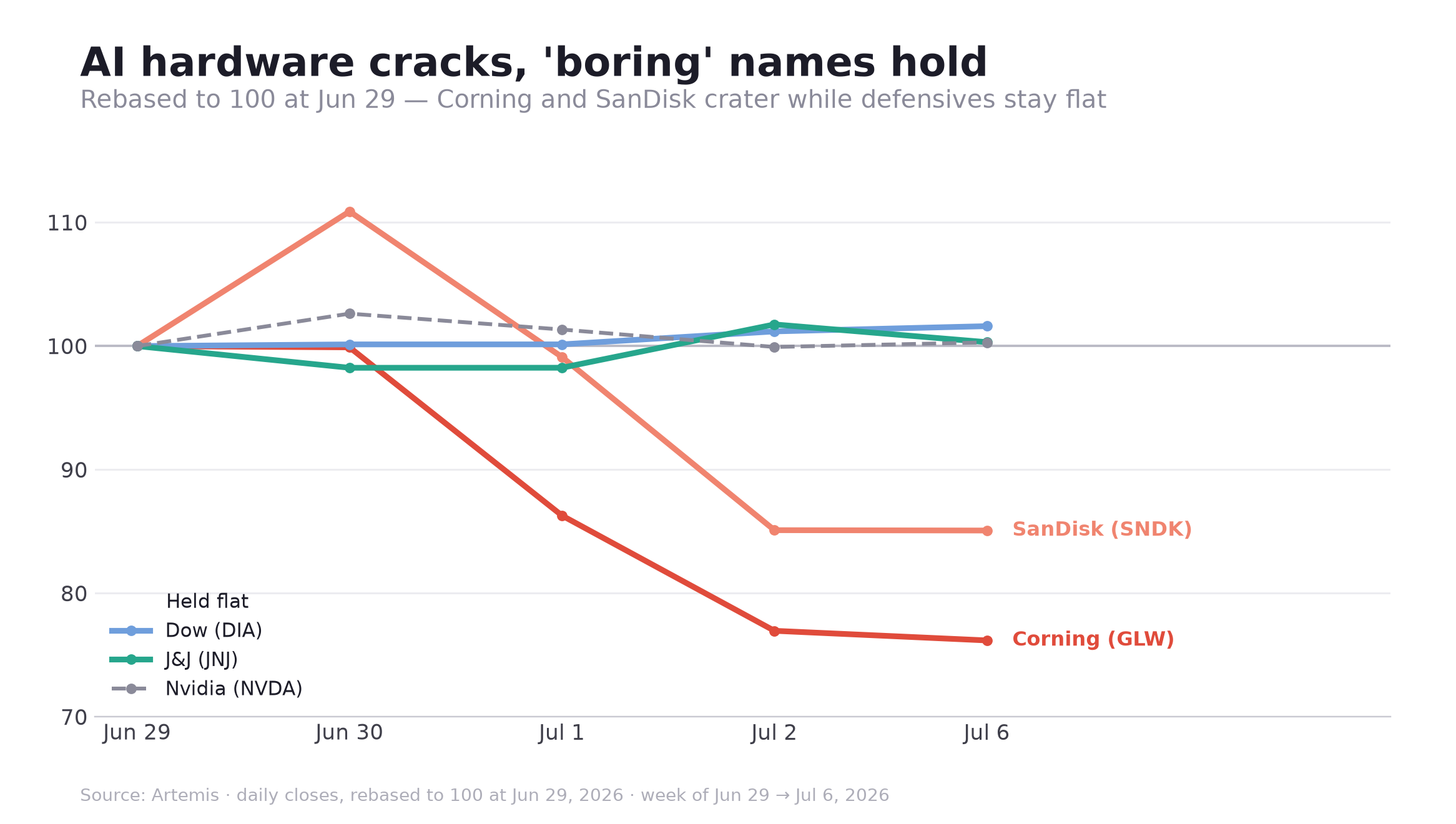

Corning fell 23.8% and SanDisk 14.9% over the week even as Nvidia and Broadcom went flat and Samsung was sold despite a record quarter. That is the signature of a positioning unwind, not a demand collapse: breadth stayed positive, the equal-weighted index held up better than the cap-weighted one, and leadership migrated toward financials, insurers, healthcare, staples and midstream energy. The Dow made records while the Nasdaq-100 slipped.

The Fed and the resumed US-Iran war are accelerants. After a hawkish June (PCE at ~4.1%, Goldman pushing its next cut to 2027), the early-July dovish inflection re-rated rate-sensitive value higher; separately, Hormuz pushed oil and the long bond up, mechanically raising the hurdle for long-duration AI winners at the worst possible moment.

Robinhood Chain: From App to Infrastructure

On July 1, Robinhood launched the public mainnet of Robinhood Chain, an Ethereum Layer-2 built on Arbitrum’s stack, purpose-built for tokenized real-world assets that trade 24/7 and plug directly into DeFi. The headline product is Stock Tokens: on-chain exposure to equities like NVDA, AAPL and GOOG, structured as tokenized debt securities (economic exposure, not legal ownership), available via the Robinhood Wallet in 120+ countries, though not the US. What sets it apart from the usual corporate-chain announcement is that a working DeFi stack was live on day one: Uniswap (a dedicated AMM as primary liquidity), Lighter, 1inch, Rialto and Arcus (from the dYdX team), with Chainlink as the official oracle. Robinhood also rolled out Earn, a Morpho-powered lending product targeting ~7% APY on USDG.

The strategic read is that this is the culmination of Robinhood’s 2025 acquisition spree (Bitstamp, WonderFi, the European tokenized-equity pilots) composed into one vertically integrated, on-chain brokerage – assets tokenized on its own network, traded through its own wallet, financed through integrated lending, custodied on its own stack. The market liked it: HOOD was one of the week’s biggest winners, up 15.4%. The open question is regulatory; the line between a compliant synthetic instrument and an unregistered security varies sharply by jurisdiction, and multiple regulators (including an SEC that just added crypto rulemaking to its July agenda) are drawing those lines right now.

Open USD: the consortium stablecoin

The week’s biggest fintech headline was the unveiling of Open USD, a new stablecoin from Open Standard — an independent venture led by former Coinbase product lead Zach Abrams and backed by a roster of roughly 140 partners that reads like a who’s-who of tech and finance: Google, Samsung, IBM, Coinbase, Solana, BlackRock, Standard Chartered, US Bank, American Express, BBVA, Visa, Mastercard, BNY and Stripe. Pitched as “a new stablecoin for global money movement… built for the internet economy,” it is set to go live later this year.

The ambition is enormous; so is the incumbency it must overcome. Stablecoin supply remains extraordinarily concentrated: on Artemis data, USDT (~$185B) and USDC (~$76B) together account for the overwhelming majority of the ~$295B+ tracked, and even well-funded fintech entrants remain small — PYUSD sits near $2.8B, Ripple’s RLUSD near $1.6B, USD1 near $4.2B. Open USD would launch into the low end of that distribution. What makes it different is distribution: a consortium spanning card networks, banks and Big Tech could route real-world payment flow to a stablecoin from day one, which is exactly the “monetization model” fintechs have been circling. It is also the clearest sign yet that stablecoins have become table stakes — the same week, Standard Chartered opened direct USDC minting/redemption for institutions via Circle, and PayPal moved PYUSD to native issuance on Polygon.

Charts of the Week

Other Notable News

DTCC began limited production trades of tokenized Russell 1000 equities, ETFs and US Treasuries in July, backed by 50+ firms (BlackRock, Goldman, JPMorgan, Circle, Ondo), with a full launch slated for October; unlike Robinhood’s synthetic model, DTCC tokenizes assets already in custody, so the tokens carry actual legal ownership

MiCA’s transitional period closed on July 1, locking Binance out of the EU after it withdrew its Greek application on June 24; capital is flowing to licensed operators, underscored by SBI’s ~$289M acquisition of Japanese exchange Bitbank — a nine-figure purchase of “permissions”

Thanks for reading! Go deeper on any story above with Artemis Analyst — our new AI analyst built on Artemis's institutional data. Ask it anything ("compare Kalshi vs. Polymarket volume," "chart spot BTC ETF flows") and get data-backed answers, comps, and charts in seconds – right in the Terminal.

Disclaimer: This newsletter is produced by Artemis for informational and educational purposes only. It does not constitute investment advice, a recommendation to buy or sell any security or digital asset, or an offer to provide advisory services. Artemis and its employees may hold positions in assets discussed. Figures are accurate to the best of our knowledge as of publication; markets move quickly.

Awesome weekly Akhil