This Week in Digital Finance

AI hardware rips to records, SoFi mints a bank-issued stablecoin, and the memory makers cross $1 trillion.

Market Overview: The Weekly Recap

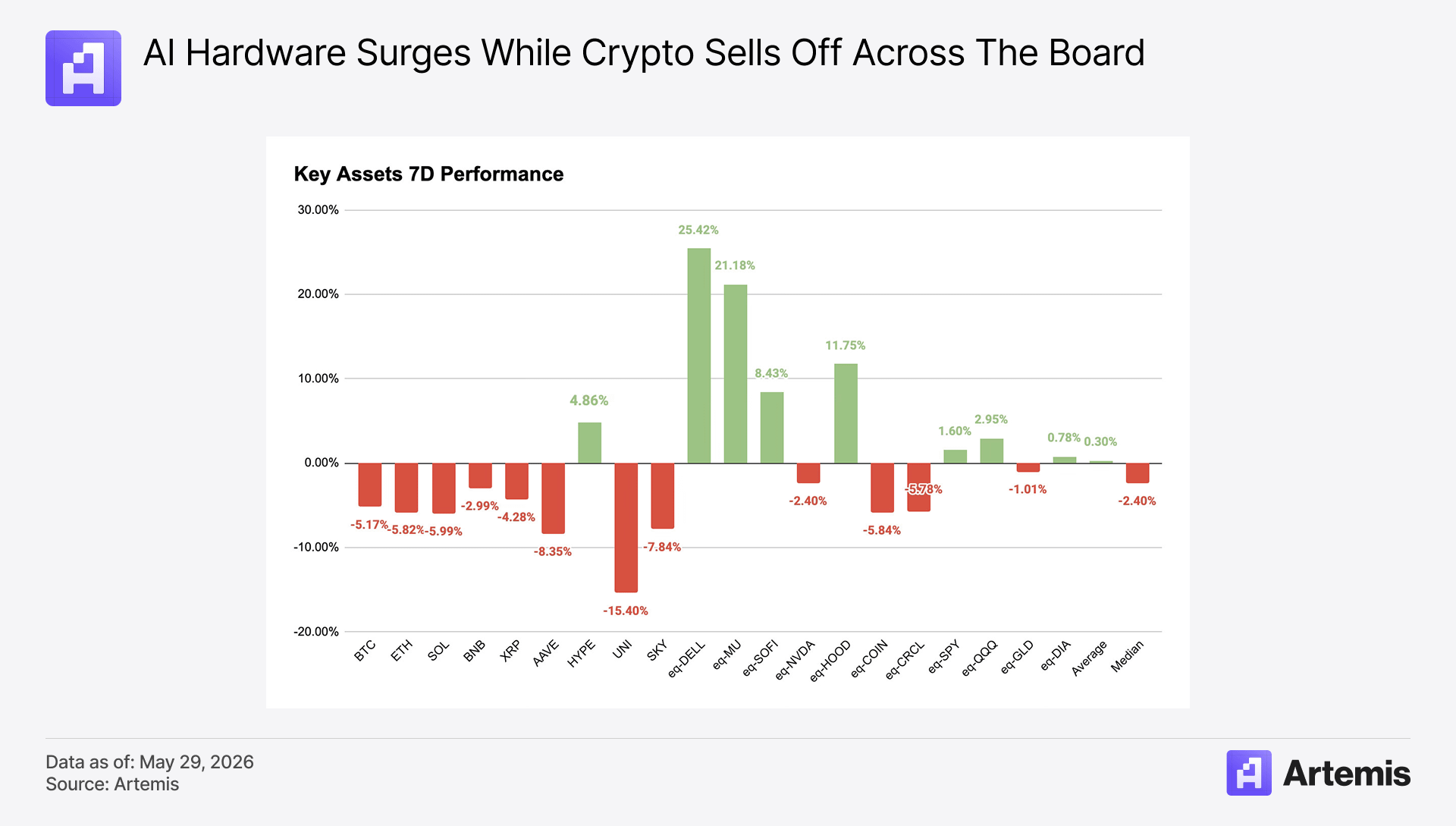

Risk assets split hard this week, with crypto taking the worst of it. US strikes near the Strait of Hormuz on May 25-26 broke the ceasefire and sent BTC below $73,000, with ETH under $2,000 for the first time since late March and the Fear and Greed Index at 22. Underneath the headlines, spot bitcoin ETFs logged a record ninth straight day of outflows, about $2.85 billion in all and the longest streak since the funds launched in January 2024.

The week split cleanly: AI hardware led while crypto fell across the board. Dell topped the basket at +25.4% on its AI-server earnings, and Micron rose 21.2% as it and SK Hynix each crossed a $1 trillion market cap, though Nvidia slipped 2.4%. Fintech was mixed, with Robinhood up 11.8% on its AI-agent trading launch and SoFi 8.4% on the SoFiUSD stablecoin, while Coinbase and Circle fell about 5.8% alongside the tokens. The major coins were uniformly lower: BTC -5.2%, ETH -5.8%, SOL -6.0%, BNB -3.0%, and XRP -4.3%, the last at its lowest since February, with UNI (-15.4%) the worst in the set. HYPE was the exception at +4.9%, holding a gain after a mid-week record near $64.63. The basket median fell 2.4% even as the S&P 500 rose 1.6% and the Nasdaq-100 2.9%.

Today We Highlight:

AI hardware ripped: Dell crushed earnings on AI servers, while Micron and SK Hynix crossed $1T market caps.

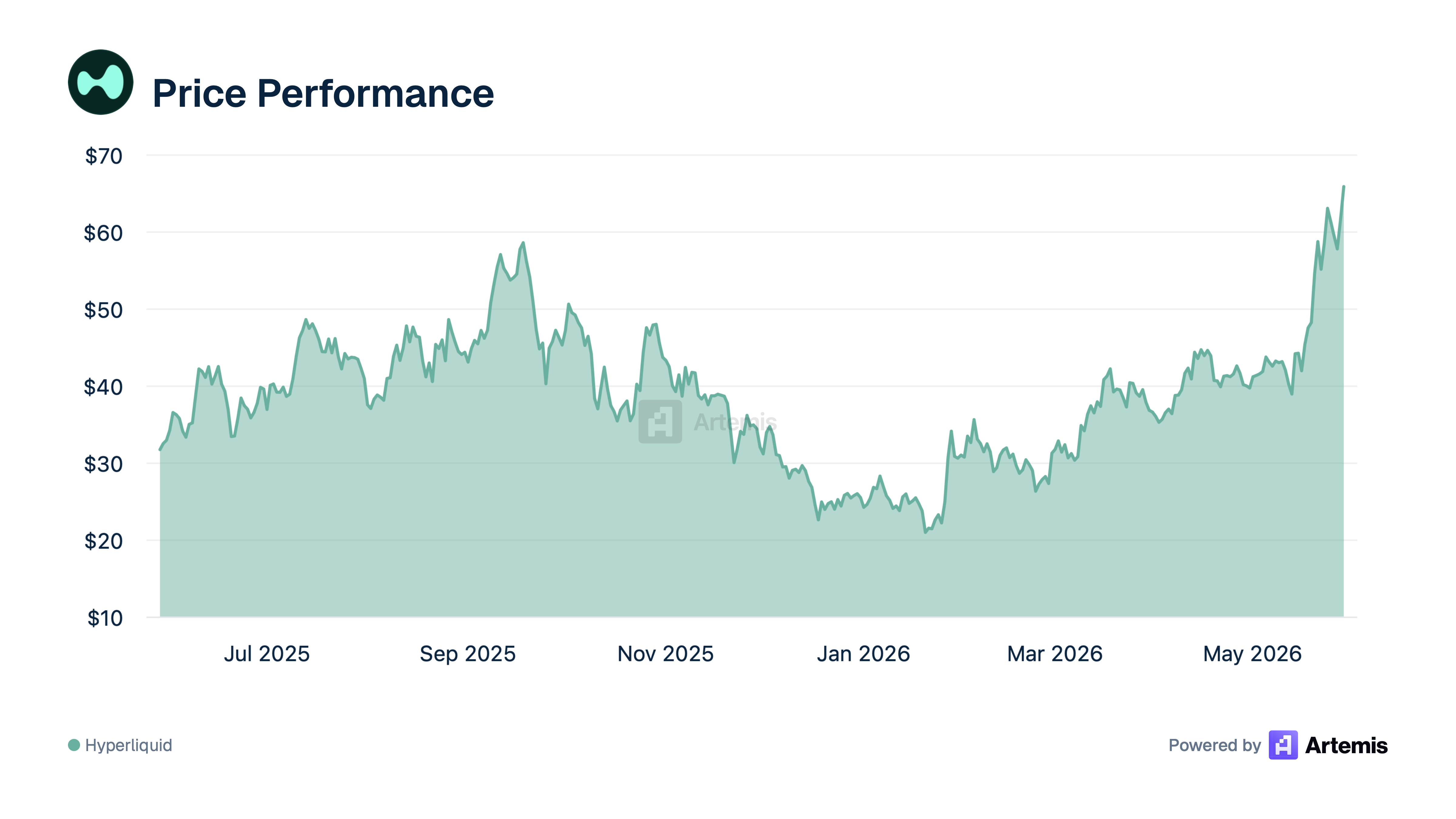

HYPE hit a record on SpaceX pre-IPO perps as private-market access moved on-chain.

SoFi launched a bank-issued stablecoin and Robinhood opened equities trading to AI agents.

ETH slid below $2,000 as a value-capture debate flared over David Hoffman’s exit and a leaner Ethereum Foundation.

1. Dell beats earnings on AI servers as Micron and SK Hynix cross $1 trillion

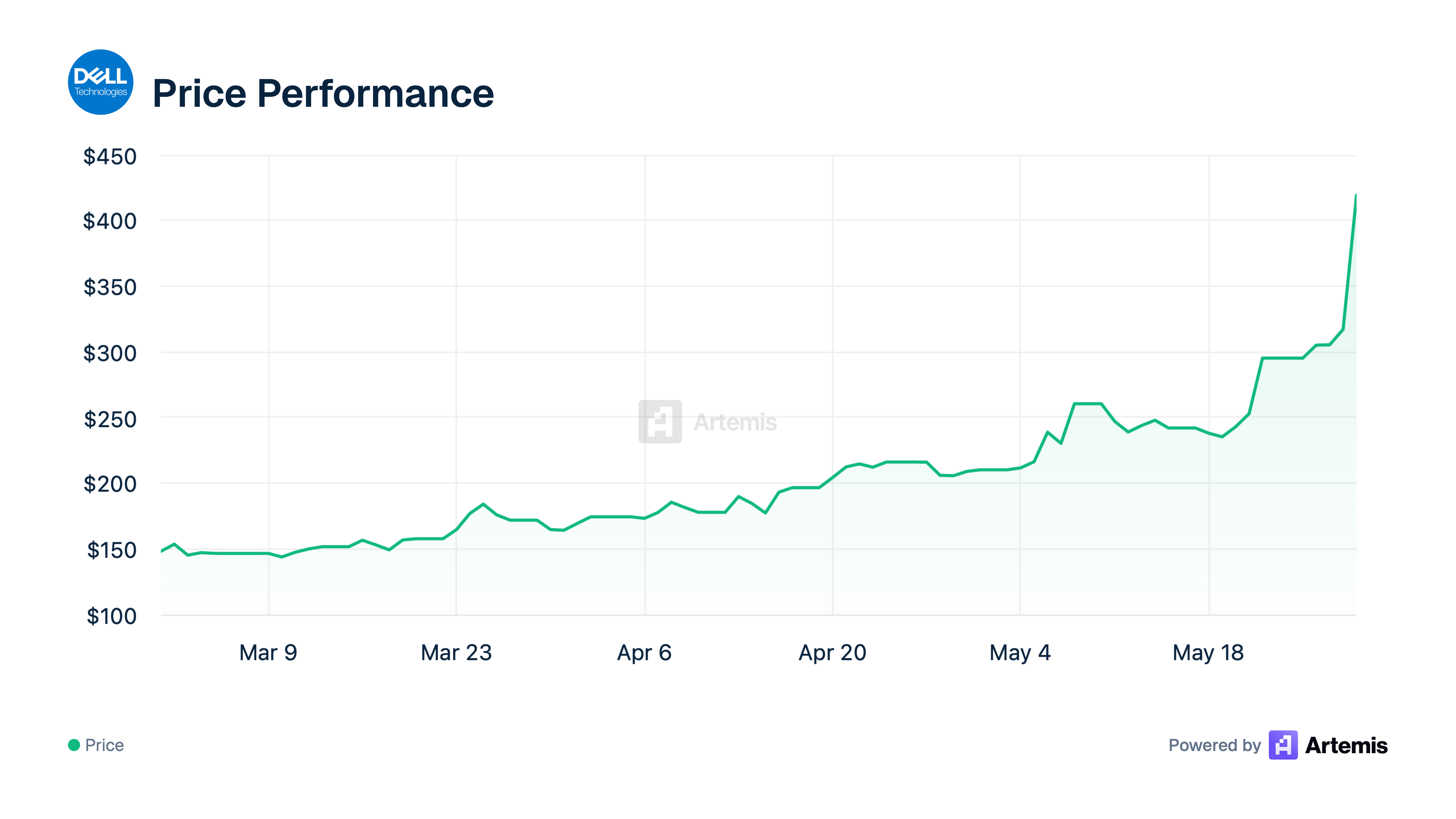

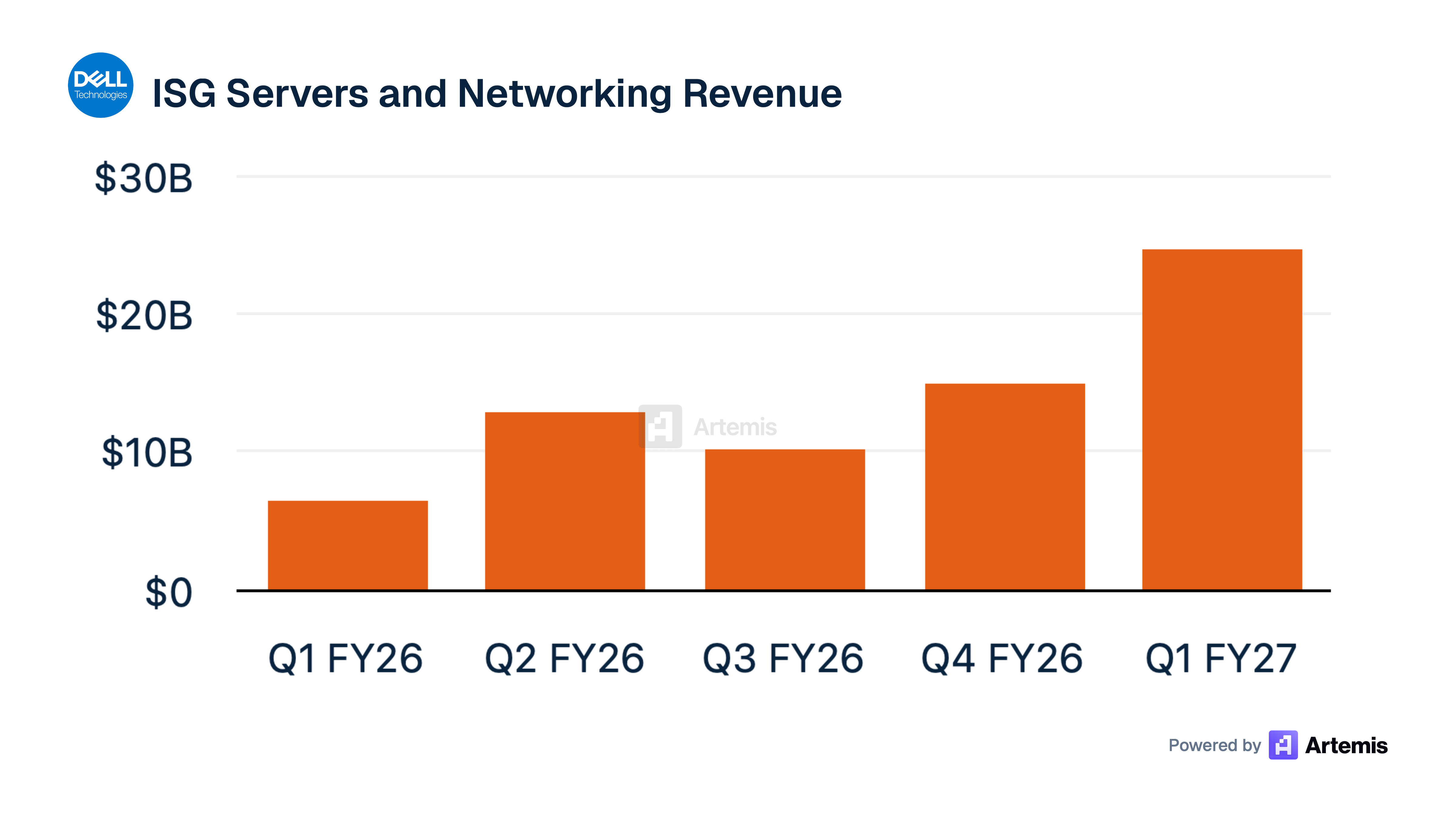

Dell reported fiscal Q1 results after the close on May 28 that reset the AI-hardware bar. Revenue of $43.84 billion grew 88% year over year, well above the roughly $35.4 billion consensus, and non-GAAP EPS of $4.86 nearly doubled the $2.94 expected. AI-server revenue rose 757% to $16.1 billion, with $24.4 billion of new AI orders booked in the quarter and a backlog of $51.3 billion. Management raised full-year revenue guidance to about $167 billion, up from a prior outlook near $140 billion, including roughly $60 billion from AI servers. The stock surged the most in two years and is up over 150% year to date. Dell separately won a $9.7 billion Pentagon software contract on Wednesday.

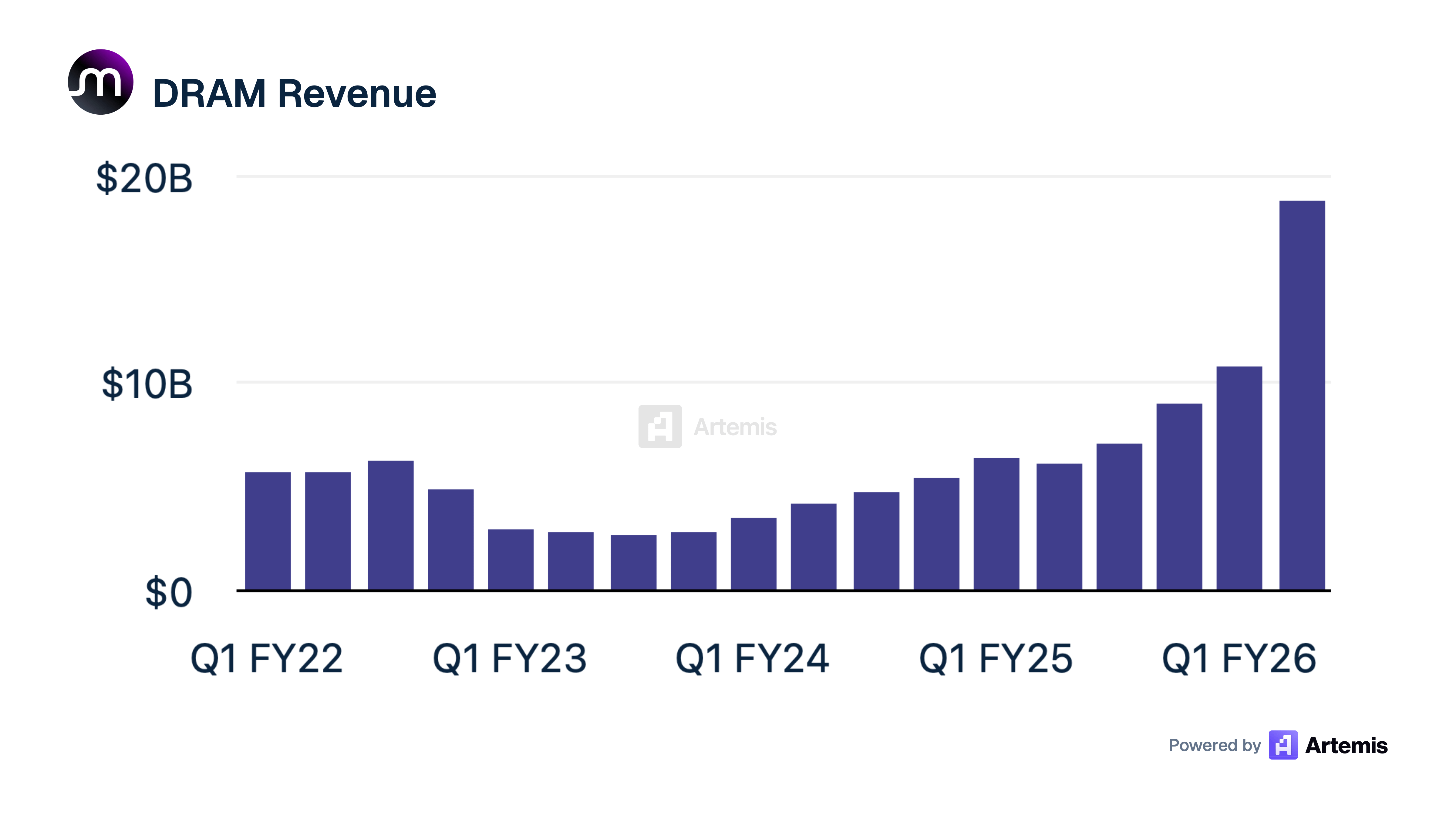

The memory side of the trade hit its own milestone. Micron and SK Hynix both crossed a $1 trillion market cap on May 27, joining Samsung, leaving the three memory makers collectively worth more than $3 trillion. The driver is a severe shortage of high-bandwidth memory and DRAM: contract prices rose roughly 90% to 95% quarter over quarter in Q1 per TrendForce, with further increases projected. SK Hynix shares have climbed more than 900% over the past year on its HBM lead. The proximate catalyst for the milestone day was a bullish UBS note, but the substance is the pricing and the sold-out capacity, not the rating change.

The strength across AI hardware traces to a single source: hyperscaler capital spending. Microsoft, Alphabet, Amazon, and Meta are on track to spend roughly $700 billion on data centers and chips in 2026, up more than 70% from 2025, and three of the four raised those budgets at their most recent earnings. That demand is why vendors like Dell and the memory makers keep beating estimates: order backlogs give forward revenue visibility, and supply stays tight enough that suppliers hold real pricing power, as the DRAM and HBM increases above show. Analysts have also repeatedly under-modeled the cycle, with Microsoft guiding 2026 capex to $190 billion against a consensus near $152 billion. The open question is durability: bulls argue the revenue growth justifies the outlay, while skeptics cite falling free cash flow, circular financing among AI firms, and valuations that leave little room for a slowdown.

2. HYPE and the race to put private markets on-chain

HYPE was the week’s most-watched crypto-native name, setting an all-time high of $64.63 on May 26 before sliding with the market to around $57 by May 28 and steadying into Friday, leaving it up about 5% on the week and outperforming the majors as bitcoin fell. The bid rested on growing institutional access. The first US spot HYPE ETFs, from Bitwise and 21Shares, launched in mid-May and drew early inflows. Around the same time, Coinbase listed HYPE and signed a USDC arrangement that lets Hyperliquid capture most of the yield on the roughly $6.8 billion of USDC held on the platform, a new recurring revenue stream. And on May 28, a Grayscale report flagged Hyperliquid as a breakout success, projecting around $800 million in annual revenue.

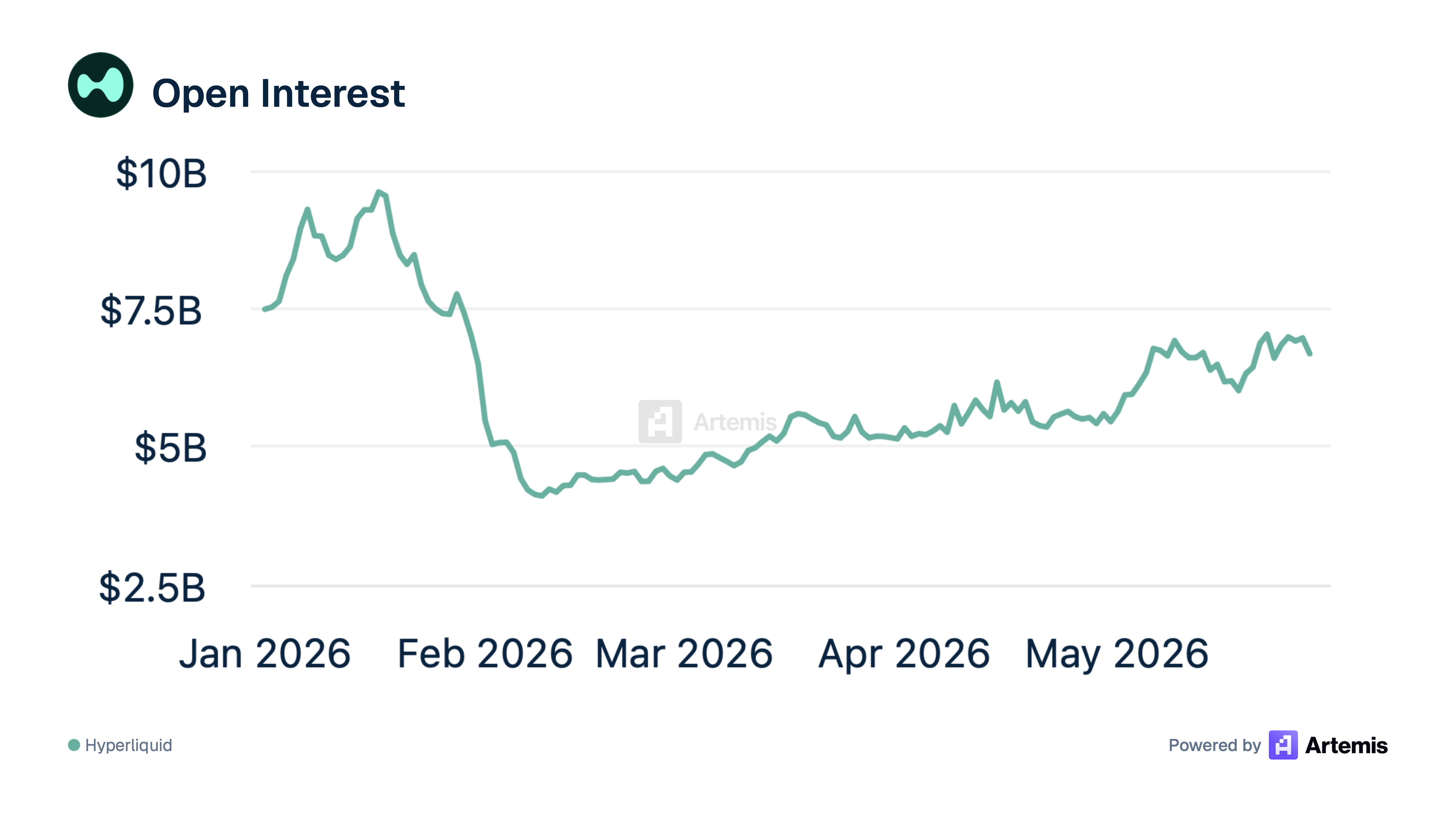

The third leg is Hyperliquid’s 24/7 commodity markets. Its permissionless HIP-3 perps have made it a round-the-clock venue for oil and metals, and during Iran flare-ups it has repeatedly captured the hedging flows that arrive when oil moves while traditional futures are closed. The volumes are real: single-day oil volume has topped $1 billion during peak volatility, and as recently as mid-May the WTI and Brent contracts carried combined open interest above $480 million, with oil at times the platform’s most active market after bitcoin. Because that activity generates fees that accrue back to the token, traders increasingly read the platform’s macro volume as a fundamentals signal for HYPE, and the same US-Iran ceasefire-extension uncertainty that pressured bitcoin this week coincided with HYPE outperforming the majors.

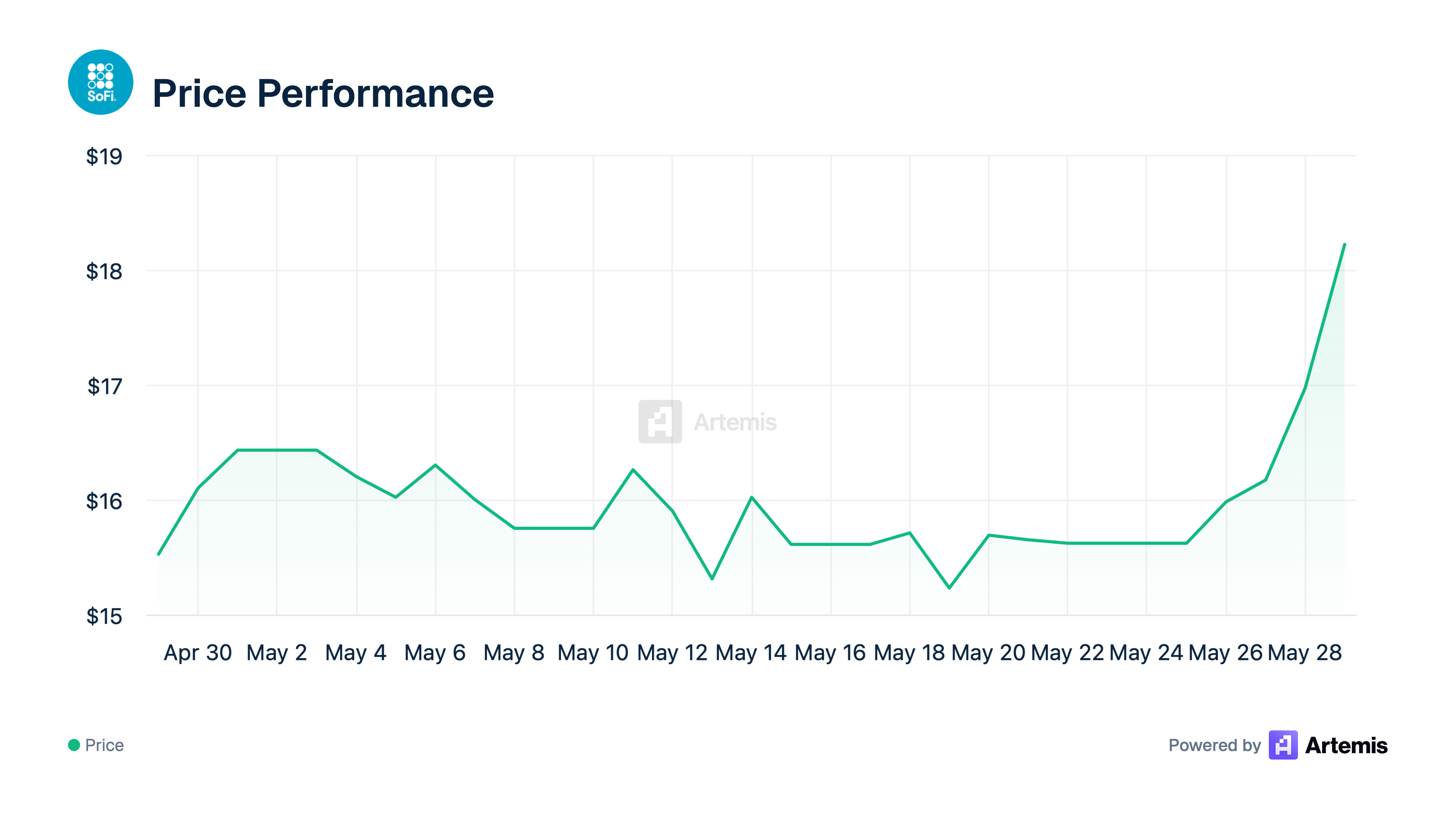

3. SoFi launches a bank-issued stablecoin: SoFiD

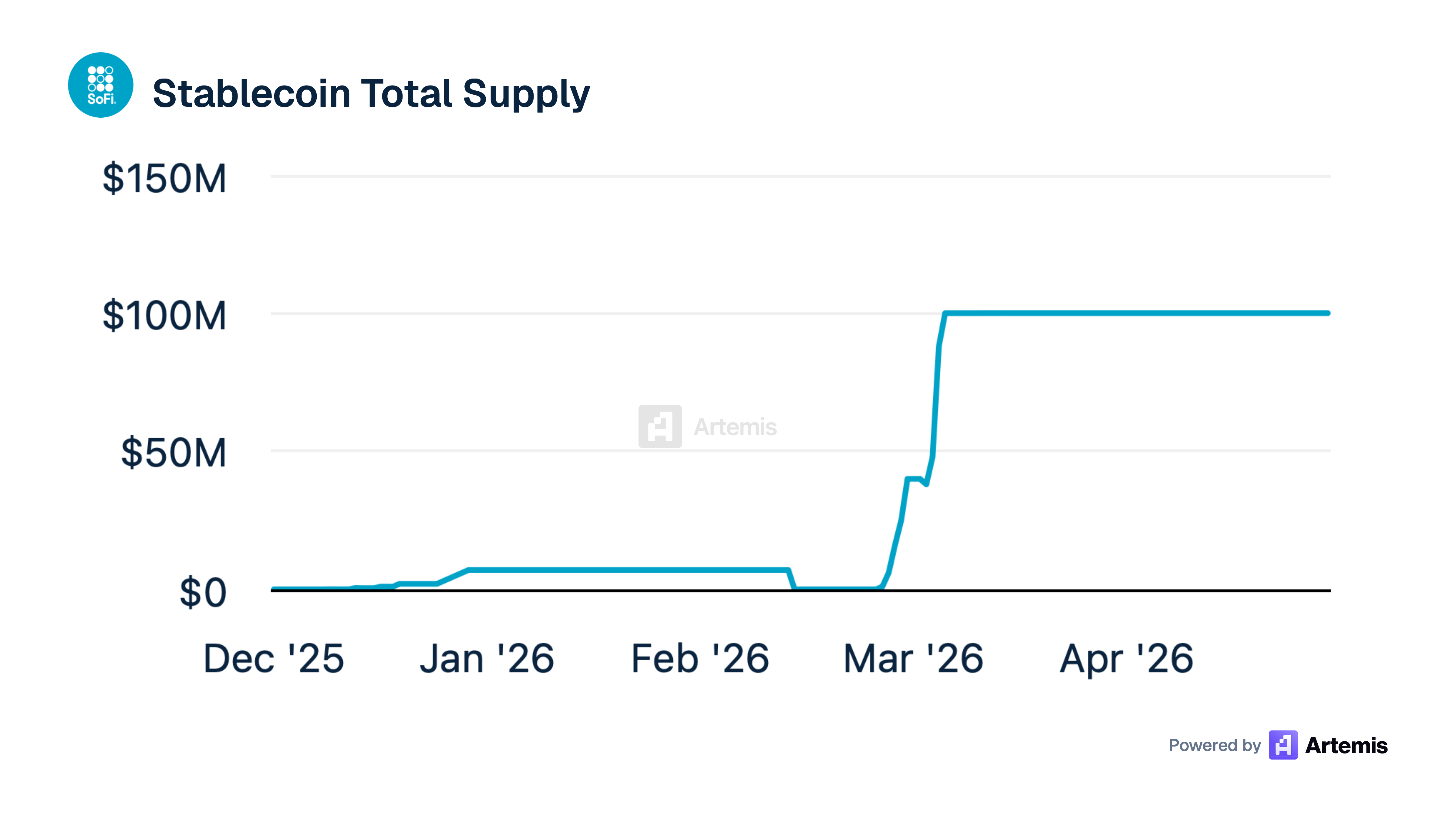

SoFi was the week’s standout fintech, up about 12% on Friday and roughly 8% on the week on the launch of SoFiUSD (ticker SoFiD), a move that lifted peers like Robinhood and Upstart and built on a record Q1 in which SoFi re-entered crypto trading. The token is a fully reserved digital dollar held against cash at SoFi Bank, built on BitGo and live on Ethereum and Solana; its roughly 15 million members can buy, sell, hold, convert, and redeem it 1:1 in the app, making SoFi the first US national bank to put its own stablecoin inside a consumer banking app.

The launch is a direct product of the GENIUS Act, the July 2025 law that lets bank units issue payment stablecoins under OCC supervision with full 1:1 reserves. Because it bans paying interest on the stablecoin itself, SoFi splits the products: SoFiUSD is a non-yield payment token that is not a deposit and not FDIC-insured, while the planned tokenized deposits are the interest-bearing, insured layer.

4. ETH's value-capture debate resurfaces as the Foundation slims down

ETH’s drop below $2,000 coincided with a resurfaced question: whether ETH the asset captures the success of Ethereum the network. Bankless co-founder David Hoffman, a longtime advocate, revealed he had sold his entire ETH after nearly nine years, teasing it May 21 and explaining it May 26: “the ETH is money thesis didn’t fail, it played out.” He stays bullish on the network but doubts ETH will be structurally rerated, since Ethereum has deliberately pushed value outward to layer-2s, apps, and stablecoins rather than capturing it at the base layer. The price reaction was muted, but the post drew over a million views and reopened the debate.

The debate overlaps with turnover at the Ethereum Foundation, where at least eight senior contributors have left or announced exits in 2026, five in May, hitting core protocol research hardest. In a May 24 post he stressed was his personal view, Vitalik Buterin defended the restructuring, describing a smaller EF that pursues “longevity over breadth,” sells less ETH, and narrows its mandate to core properties he labels CROPS: censorship and capture resistance, openness, privacy, and security. He noted the EF holds only about 0.16% of all ETH and that 90% of his net worth sits in it. Selling less eases a supply complaint but does not settle the value-capture question, and some read his neutral-infrastructure framing as confirming the gap Hoffman flagged, even as plenty of analysts still see upside from upgrades and ETF demand.

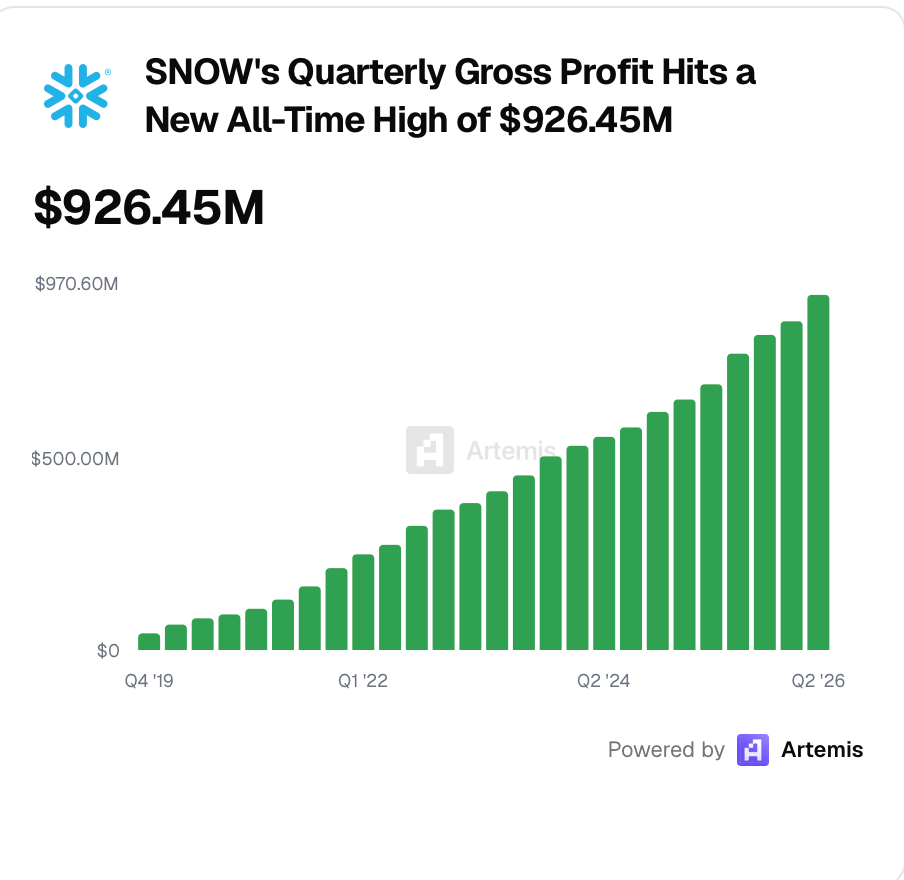

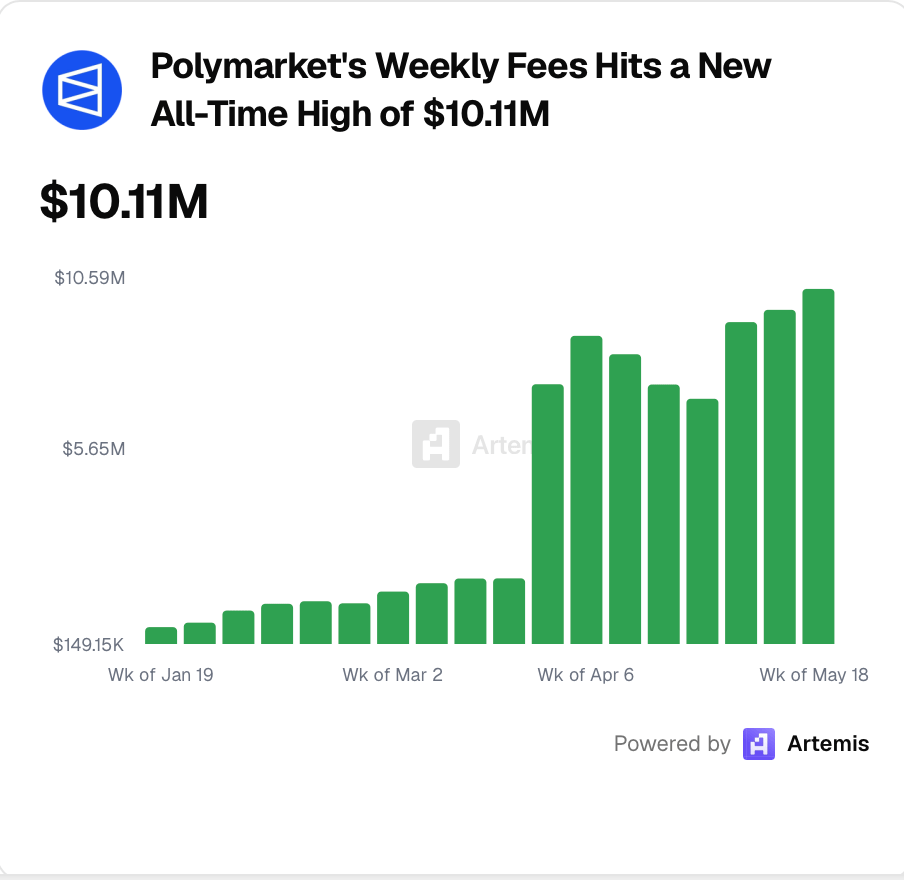

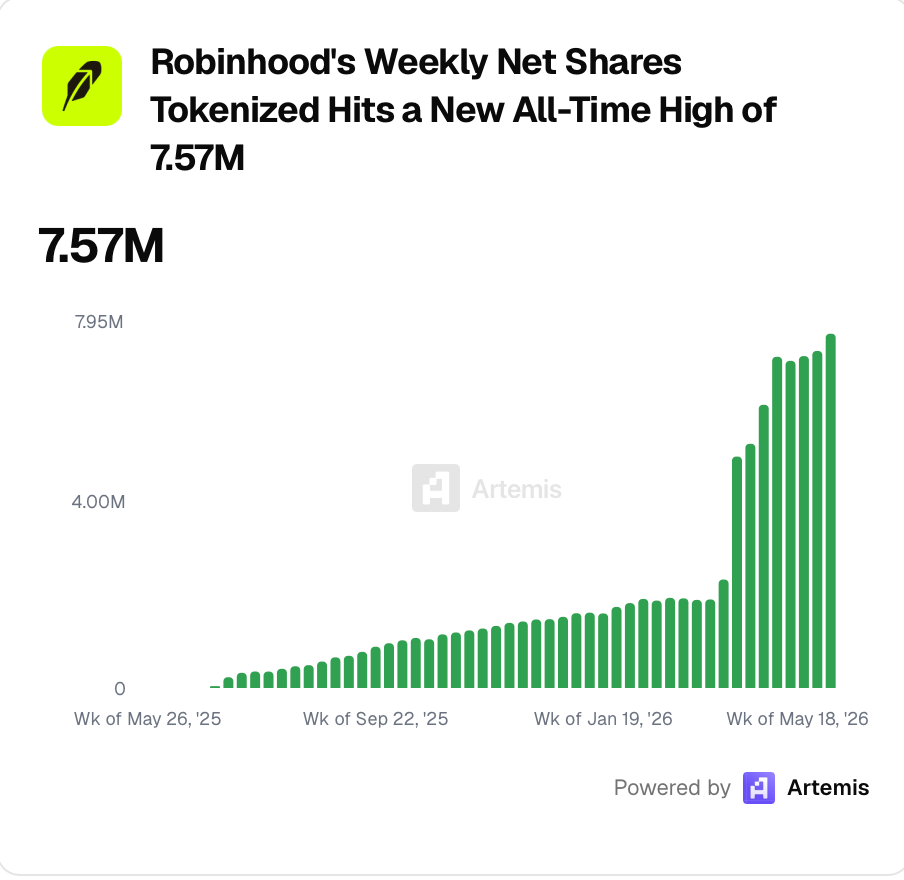

Charts of the Week

Courtesy of Artemis Insights

Thanks for reading! Stay ahead this week by using the Artemis Terminal to pull the underlying data on any of the stories above (CLARITY Act vote tracker, COIN Q1 segment revenue, USDC supply on Hyperliquid) or pull live numbers straight into your models with =ART() in Excel.

Disclaimer: This newsletter is produced by Artemis for informational and educational purposes only. It does not constitute investment advice, a recommendation to buy or sell any security or digital asset, or an offer to provide advisory services. Artemis and its employees may hold positions in assets discussed. Figures are accurate to the best of our knowledge as of publication; markets move quickly.

Lets go Akhil