This week in Digital Finance

Bitcoin logs its worst week since February and Broadcom's blowout isn't enough

Market Overview: The Weekly Recap

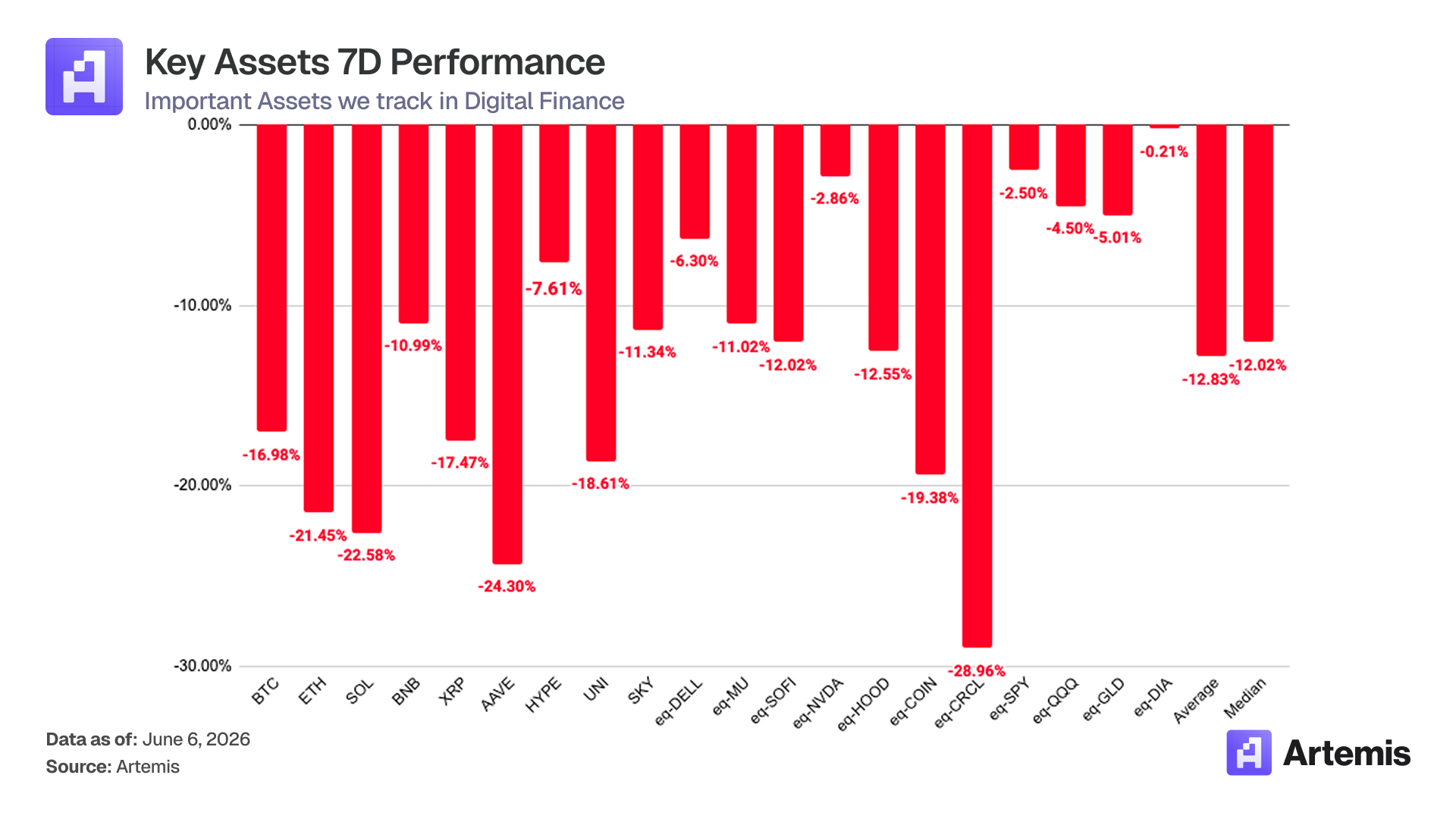

Risk assets reversed hard this week, with crypto taking the worst of it by a wide margin. A blowout May jobs report on June 5 (172,000 jobs against ~80,000 expected) flipped the Fed conversation from cuts to hikes and spiked Treasury yields, while Broadcom's soft AI-chip guide two days earlier had already snapped a nine-week equity win streak and triggered the Nasdaq's worst day since April 2025 (down -4.18%). BTC fell to $59,000 (at it lowest), its worst week since February, ETH broke $1,500 for the first time since spring, and the Crypto Fear & Greed Index collapsed to 16 (Extreme Fear) from 42 (Greed) a week ago. Underneath the headlines, spot bitcoin ETFs extended a record outflow streak to about $4 billion since mid-May.

The week split cleanly, and it inverted last week's: the names that led the rally now led the defense, while crypto cratered. Equities and havens held up best: DJIA -0.2%, SPY -2.5%, NVDA -2.9%, QQQ -4.5%, and gold (GLD) -5.0%, with Dell giving back part of last week's surge at -6.3%. The crypto-equity complex was hit far harder: SoFi -12.0%, Robinhood -12.6%, Coinbase -19.4%, and Circle the single worst name in the basket at -29.0%. The major coins were uniformly lower: BTC -17.0%, ETH -21.5%, SOL -22.6%, BNB -11.0%, and XRP -17.5%, with the DeFi names worst of all (AAVE -24.3%, UNI -18.6%). HYPE was the relative standout at -7.6%, the most resilient crypto in the set even after a mid-week record near $75.51 gave way. The basket median fell 12.0% (average -12.8%), with even the S&P 500 (-2.5%) and Nasdaq-100 (-4.5%) holding up far better than anything in crypto.

Today We Highlight:

Strategy sold bitcoin for the first time in four years, a trivial 32-coin sale that reframed the whole selloff as a rotation into AI.

Coinbase launched SpaceX pre-IPO perps days before the largest IPO in history, pushing private-market access further on-chain.

HYPE’s win streak ended, but at -7.6% it was still the most resilient crypto in the basket as the majors fell 17-24%.

The nine-week equity win streak snapped: Broadcom beat but guided soft on AI chips, sending the Nasdaq to its worst day since April 2025.

1. Strategy sells bitcoin, and the rotation thesis goes mainstream

For four years Michael Saylor’s promise was unconditional: Strategy buys bitcoin and never sells. On June 1 an 8-K ended that streak. The company disclosed selling 32 bitcoin between May 26 and 31 at an average of $77,135, about $2.5 million, to help fund the dividend on its STRC perpetual preferred (”Stretch”). It was Strategy’s first bitcoin sale since December 2022.

Thirty-two coins is roughly 0.0038% of the 843,706 BTC Strategy still holds at a blended cost near $75,699, a ~$63.8 billion position. In the same week the company raised $128.3 million through its at-the-market equity program (fifty times the size of the bitcoin sale) and continued buying back its 2029 convertible notes. TD Cowen and others called the sale economically immaterial, a tactical move to service preferred dividends rather than a change of heart. Markets disagreed on the meaning: MSTR fell about 5% on the disclosure, bitcoin slipped to a near two-month low, and the move revived old questions about the digital-asset-treasury model now that most DAT peers have halted purchases or turned net sellers since October. With BTC well below Strategy’s cost basis, the firm is sitting on a paper loss north of $11 billion, and a June 8 shareholder vote on capital-structure matters will test how the narrative holds with institutions.

The more useful signal came from Saylor’s own framing. Rather than defend a price, he reframed the entire selloff as a rotation: he argues AI infrastructure is pulling in roughly $400 billion of investment over six months, and that the ~$4 billion of bitcoin ETF outflows since mid-May reflect capital migrating into that trend rather than a verdict on bitcoin’s fundamentals. Bitcoin is now trailing equities by the most since 2019, and the newest products being built (pre-IPO and AI exposure, not spot crypto) are following the same capital. The DAT model was the 2024-25 vehicle for “leveraged bitcoin beta.” In 2026 the market is asking these companies to earn their keep, and the capital that once chased mNAV premiums is shopping elsewhere.

Analyst Take: I think Saylor’s selling Bitcoin is a net positive for both MSTR 0.00%↑ and the market. It finally puts the balance sheet to work rather than leaving it as unrealized optionality, a pile of what it "could be." The sales give Strategy a cleaner way to fund its preferred dividends, and when mNAV falls below 1, to buy back its own shares, which lifts bitcoin per share.

2. Coinbase puts private markets onchain, just in time for the largest IPO ever

Last week we wrote about the race to put private markets on-chain. This week Coinbase made it a product.

On June 4, Coinbase launched its first pre-IPO perpetual futures on its international exchange, listing SpaceX (ticker SPCX-PERP) as the inaugural underlying. The contracts are USDC-settled, trade 24/7 with no expiry, offer up to 5x leverage, and are available to eligible users outside the US through Coinbase’s Bermuda entity. The design is the interesting part: because a private company’s full share count isn’t public, the contract references a valuation-based index rather than a share price: a quote of 1,735 implies a $1.735 trillion equity valuation. When SpaceX completes its IPO, Coinbase pauses trading and rebases the contract into a standard per-share equity perp via a P&L-neutral adjustment.

The timing is not accidental. SpaceX filed Amendment No. 1 to its S-1 on June 1, setting a roadshow price of $135 per share and a plan to sell 555.6 million shares to raise roughly $75 billion at a valuation near $1.75 trillion, which would make it the largest IPO in history, more than double Saudi Aramco’s 2019 record. The roadshow began June 4; pricing is expected around June 11 with a Nasdaq debut targeted for June 12. Coinbase isn’t first or alone here: Binance launched pre-IPO perps on May 21, and Ventuals has run the same playbook on Hyperliquid’s HIP-3 for months.

3. HYPE’s win streak ends, but it still won the week

For a month, Hyperliquid was the answer to the question of what’s working, the one major crypto asset printing new highs while everything else bled. This week the exception ended.

HYPE set a fresh all-time high around $75.60 on June 3, extending a roughly 26% monthly run built on the Coinbase/Circle USDC alignment, ETF launches from Bitwise and 21Shares, DAT accumulation, and genuinely strong perp and HIP-3 volumes. Then it reversed with the rest of the market, sliding more than 20% from that Tuesday peak. Two name-specific headlines didn’t help: the UK’s FCA issued an unauthorized-firm warning on the platform, and BitMEX co-founder Arthur Hayes disclosed exiting his entire HYPE position, both landing June 5 into an already-fragile tape. And yet, here is the part that matters: HYPE finished the week down just 7.6%, the best-performing crypto asset in our basket on a week when BTC fell 17%, ETH 21%, and SOL 23%. The win streak ended; the relative outperformance did not.

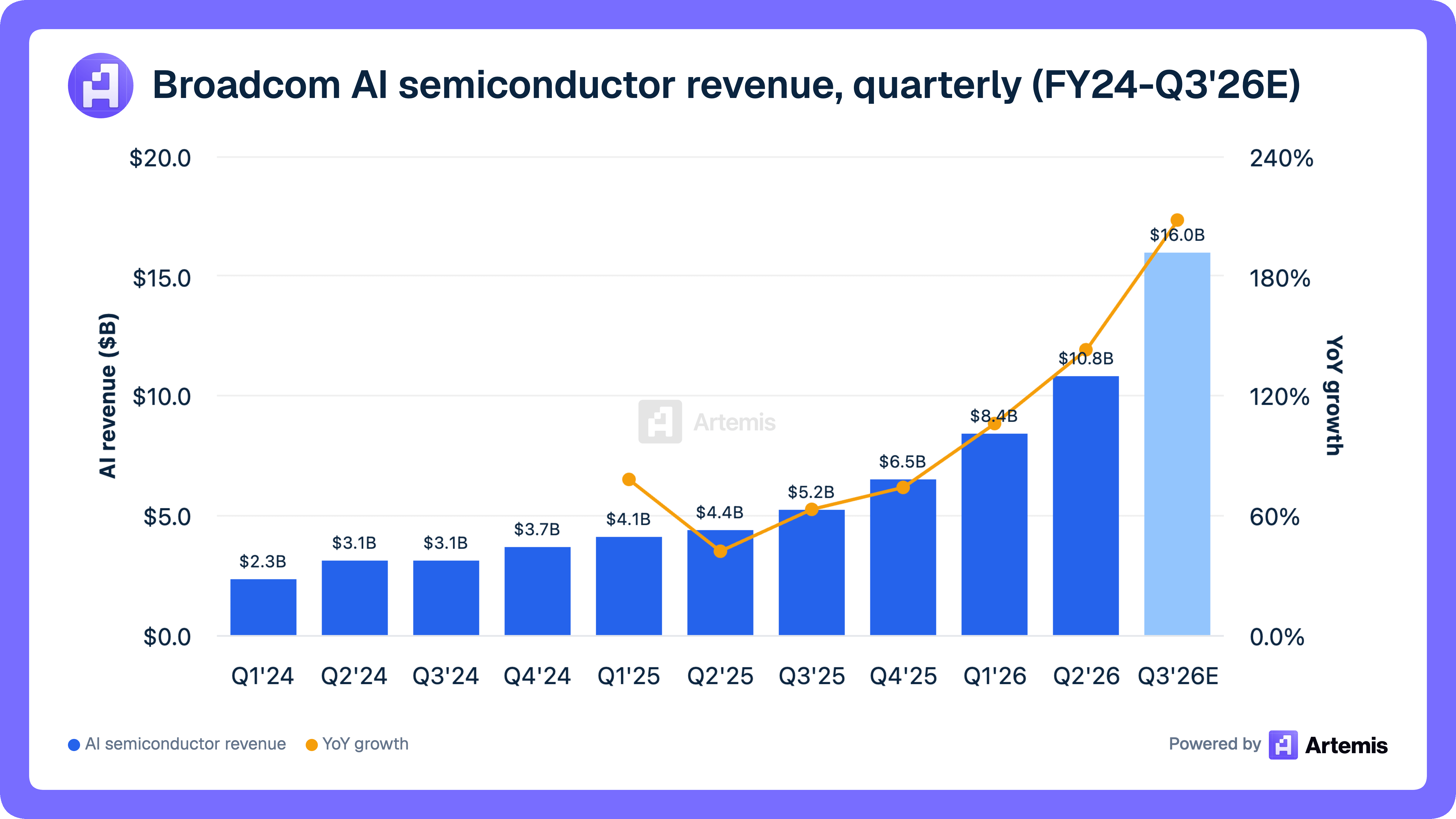

4. Broadcom beat, and the nine-week streak broke anyway

Why does a company grow AI revenue 143% year over year, beat on both lines, and lose a sixth of its value in two sessions?

Broadcom’s fiscal Q2 (reported June 3 after the close) was strong by any normal standard: revenue of about $22.2 billion edged consensus, non-GAAP EPS of $2.44 beat the $2.39 estimate, and AI semiconductor revenue grew 143% to $10.8 billion. Current-quarter total revenue guidance of $29.4 billion also came in above the Street. The problem sat entirely in one line. Management guided fiscal Q3 AI chip revenue to $16 billion against a roughly $17.2 billion consensus and, critically, left the full-year AI target at $56 billion rather than raising it. After first-half AI revenue approached $19 billion, investors had penciled in an upgrade. When the math landed at a ceiling instead of a floor, it triggered a textbook sell-the-news reaction. Two remarks on the call deepened it: Hock Tan acknowledged Google would likely use multiple chip suppliers, and he flagged that the AI mix is diluting gross margins. AVGO, which had entered the print at an all-time high up ~40% YTD, was downgraded to Neutral and fell roughly 14% Thursday before sliding further Friday to close near $386.

The read-through mattered more than the name. Broadcom is the cleanest proxy for hyperscaler custom-silicon demand, building accelerators for six of the largest buyers, including Google, Meta, OpenAI and Anthropic, on 18-to-24-month design cycles that lock customers in. If even Broadcom’s forward guide can’t clear a raised bar, the entire group is vulnerable to the same gravity. Nvidia fell 6% on Friday alone, with AMD, Micron and Intel following, though on a full-week basis the megacaps proved far more resilient than the single-day carnage implied (NVDA -2.9%, versus memory names like Micron down ~11%).

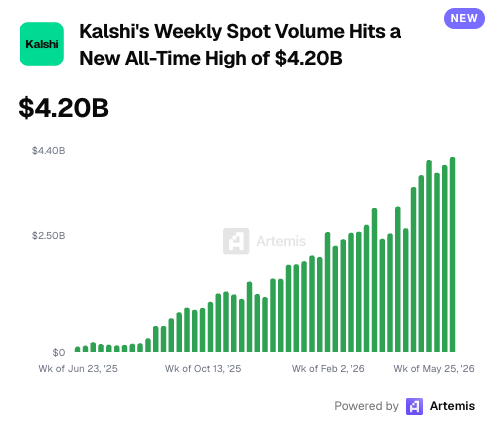

Charts of the Week

Courtesy of Artemis Insights

Other Notable News

MoneyGram launched MGUSD on Stellar on June 2, a native USD stablecoin issued by Stripe-owned Bridge (GENIUS Act-ready), with M0 minting infrastructure and Fireblocks custody. Targets MoneyGram’s 60M+ customers and ~500,000 retail locations, US-first with global rollout planned, the latest legacy remittance player onto stablecoin rails after Western Union’s USDPT.

Morgan Stanley and Galaxy Digital opened a crypto-to-ETP lending path on June 5: eligible wealth clients can lend BTC, ETH, or SOL to Galaxy for spot crypto ETP shares (including MSBT) without triggering a taxable sale. Galaxy cut its Morgan Stanley-referral minimum from $25M to $5M, with onboarding times projected down up to 75% from 4-plus weeks.

Mastercard opened card settlement to six regulated stablecoins across eight chains on June 3 (Ethereum, Solana, Polygon, Base, Arbitrum, XRPL, Canton, Tempo), adding intraday, weekend, and holiday windows. Visa expanded to nine chains in April at a ~$7B settlement run-rate, +50% QoQ.

Stripe, Visa, and Mastercard neared a joint stablecoin platform on June 3, with Coinbase weighing participation: a direct challenge to the Circle/Tether duopoly (~80% of the ~$325B stablecoin market) backed by distribution across 200+ countries. Coinbase's role is complicated by its USDC revenue-share with Circle.

Thanks for reading! Stay ahead this week by using the Artemis Terminal to pull the underlying data on any of the stories above (COIN segment revenue and pre-IPO perps volume, spot BTC ETF flows, HYPE fees and buybacks) or pull live numbers straight into your models with =ART() in Excel/Google Sheets.

Disclaimer: This newsletter is produced by Artemis for informational and educational purposes only. It does not constitute investment advice, a recommendation to buy or sell any security or digital asset, or an offer to provide advisory services. Artemis and its employees may hold positions in assets discussed. Figures are accurate to the best of our knowledge as of publication; markets move quickly.