This Week in Digital Finance

Week ending Tuesday, April 28, 2026

Market Overview: The Weekly Recap

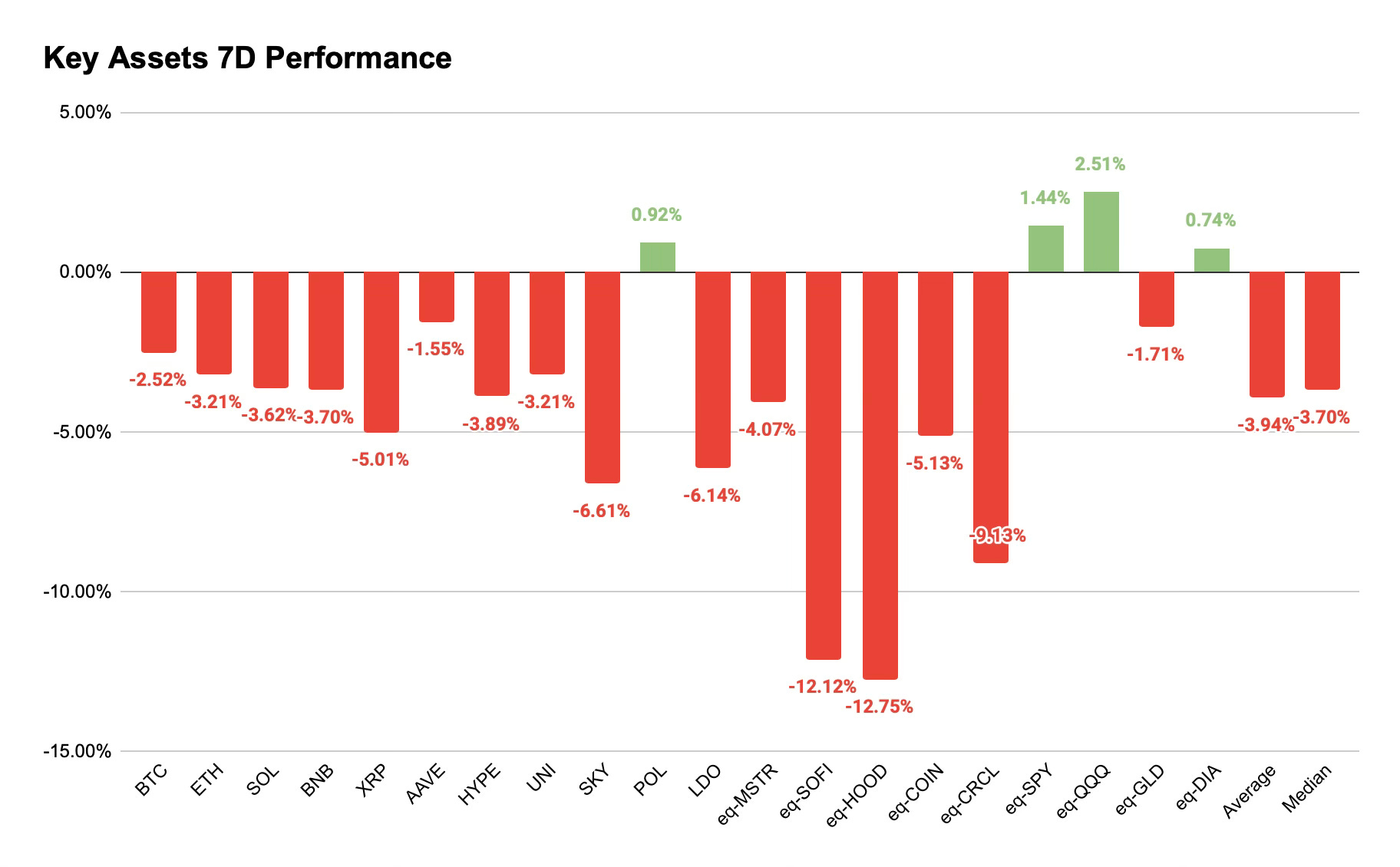

Crypto and crypto-equities took the worst of last week’s risk-off move, with the basket median printing -3.70% and crypto-fintechs HOOD (-12.75%), SOFI (-12.12%), and CRCL (-9.13%) leading the drawdown. Traditional equities went the other way, with QQQ +2.51% and SPY +1.44% on the megacap earnings cluster, leaving crypto distribution names repriced harder than the underlying assets they trade. The macro backdrop turned hawkish into the move: headline PCE printed 3.5% YoY on April 30, the hottest reading since May 2023, and the FOMC held rates at 3.5% to 3.75%. U.S. spot Bitcoin ETFs flipped to three consecutive days of net outflows totaling roughly $491M into FOMC week. BTC closes the period near $76,300, having stalled twice at $80,000 resistance.

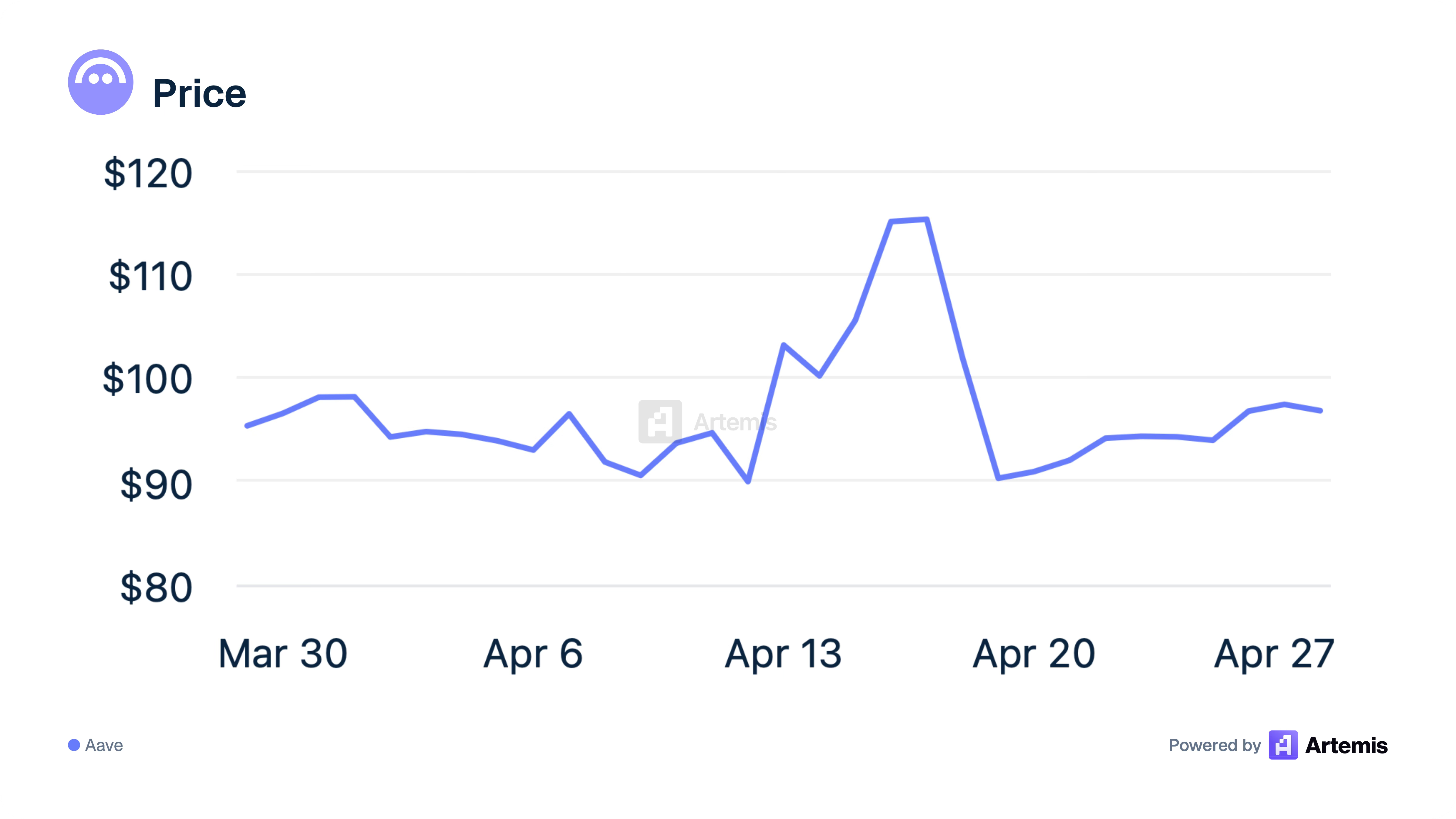

In the basket, POL (+0.92%) was the only green crypto print as Polygon picked up Meta, Visa, and Modern Treasury USDC integrations. AAVE (-1.55%) held up best in major DeFi on the DeFi United bailout proposal, while SKY (-6.61%) and LDO (-6.14%) gave back the prior week’s gains from the Treasury Management Function proposal and the $20M LDO buyback program respectively. The L1 majors traded in a tight band: BTC -2.52%, ETH -3.21%, SOL -3.62%, BNB -3.70%, with XRP at -5.01% the laggard. Among equities, eq-MSTR (-4.07%) tracked BTC’s stall, while the crypto-distribution names carried the heaviest losses on combined earnings disappointment and risk-off sentiment

Today We Highlight

Robinhood and SoFi both reported revenue beats overshadowed by softer forward color; HOOD fell 12.75%, SOFI fell 12.12%.

Polygon picked up Meta, Visa, and Modern Treasury USDC integrations in the same week Polymarket signaled chain migration.

Strategy extended weekly BTC accumulation to four straight weeks, adding 3,273 BTC for $255M and bringing total holdings to 818,334 BTC.

Aave service providers proposed “DeFi United” with Lido and EtherFi to cover KelpDAO bridge losses; AAVE held up best in major DeFi at -1.55%.

1. Robinhood and SoFi: earnings get repriced

Robinhood and SoFi both reported Q1 earnings the week of April 28, and both stocks sold off sharply despite topline growth. HOOD finished -12.75% on the week and SOFI -12.12%. The two prints share a common pattern: revenue held up across deposits, lending, and equities, but crypto-tied revenue contracted and the market repriced both names off their crypto-cycle multiples.

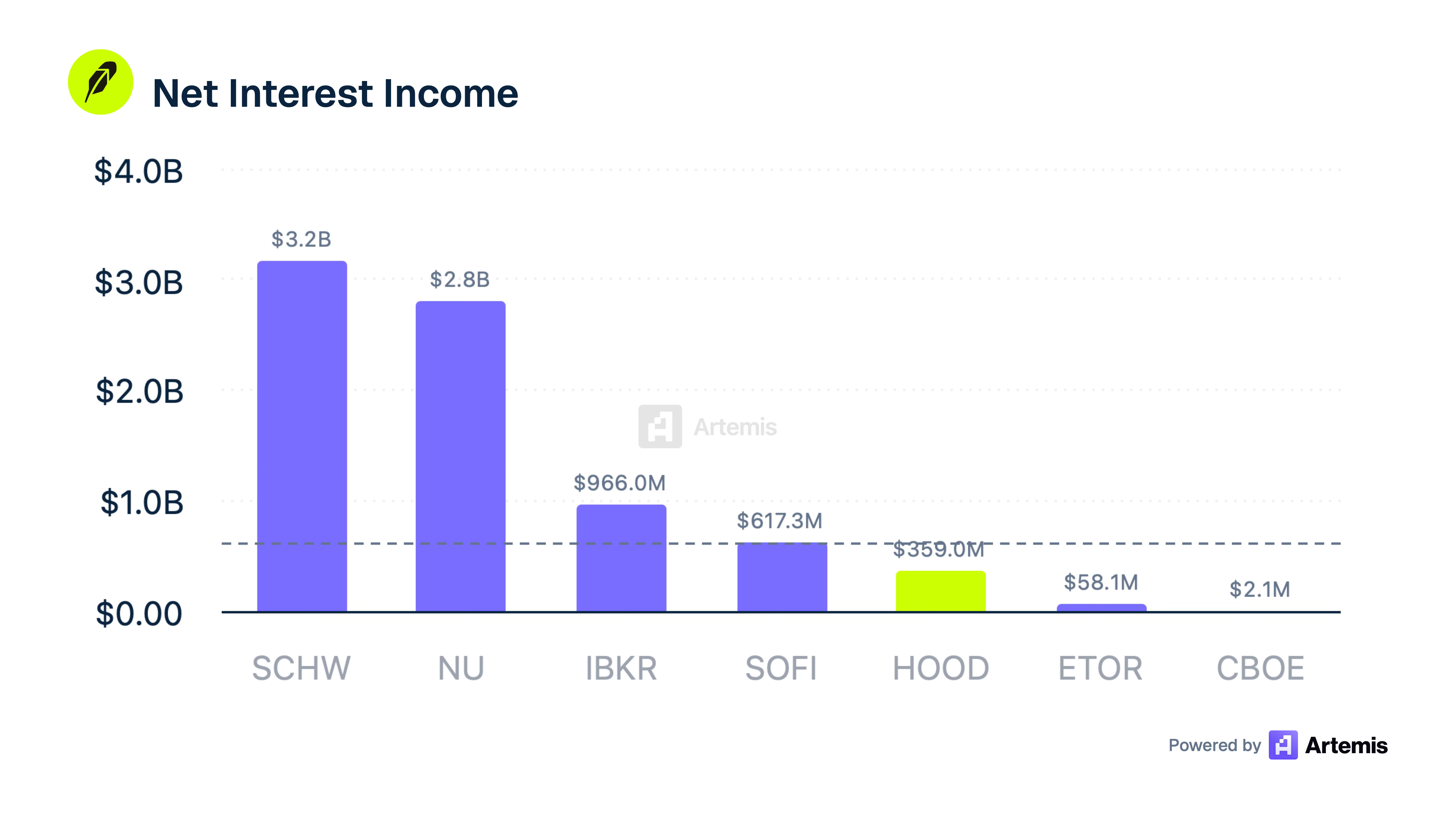

Robinhood missed on net revenue ($1.07B vs $1.14B consensus) and EPS ($0.38 vs $0.39), with the miss driven by crypto revenue falling 47% YoY to $134M on just $24B of notional volume. Equities revenue grew 46% to $82M, event contracts jumped 320% to $147M on a record 8.8B contracts, and net interest income added $359M (+24%). HOOD closed -13.24% on April 29 on volume 132% above average; Barclays and KBW both cut price targets. SoFi delivered record adjusted net revenue of $1.1B (+41% YoY) and a 31% EBITDA margin, but EPS of $0.12 came in line and ended a streak of beats. The selloff came from softer forward guidance, a 27% drop in Galileo platform revenue tied to Chime exiting, and credit metrics drifting the wrong way (personal and student loan charge-offs both ticking up). SoFi formally launched crypto trading on the platform during the quarter; CEO Anthony Noto called digital assets a strategic priority going forward.

Both companies are still executing on their core franchises and both have credible crypto growth ahead of them, including SoFi’s just-launched trading product and Robinhood’s tokenized stocks rollout. The question for the multiple is not whether crypto revenue recovers but how soon. Coinbase’s May 7 print will set the near-term ceiling on how the market values that recovery.

2. Polygon adds Meta and Visa, faces Polymarket migration

POL was the only token in the crypto basket to print green on the seven-day FOMC tape, closing +0.92% against a basket median of -3.70%. Polygon picked up USDC integrations from Meta, Visa, and Modern Treasury in the same week Polymarket signaled it intends to migrate off the chain.

The catalyst side. On April 29, Meta launched USDC creator payouts via Stripe, settling on Solana and Polygon. The product is live for creators in Colombia and the Philippines, with expansion to 160+ countries planned by year-end per Polygon Labs. Meta paid creators roughly $3 billion through monetization programs in 2025; even a small fraction moving on-chain meaningfully expands the surface area for USDC outside the U.S. This is Meta’s first stablecoin product since shelving Diem in 2022, and the strategic shift is that Meta is using a regulated third-party stablecoin (USDC) under the post-GENIUS Act framework rather than building its own.

The same week, Visa added Polygon to its stablecoin settlement program alongside four other networks. Visa’s stablecoin network is now running at $7B in annualized transaction volume and growing approximately 50% QoQ, implying a near-term run rate above $10B. Modern Treasury added USDC on Polygon to its Payments API. The chain itself ran roughly $37B in stablecoin volume over the trailing 30 days and generated $11M in Q1 network revenue, up from $2.1M the prior quarter.

The migration side. On April 24, Polymarket VP of Engineering Josh Stevens posted on X that “chain migration” is now a roadmap priority, citing insufficient block space, gas costs, and block times on Polygon. No target chain has been announced; an Ethereum L2 called “POLY” was on the table in December 2025, but Stevens did not confirm whether that remains the plan. Polymarket generates $2.5M to $4M in weekly fees on Polygon, accounting for 50% to 70% of the chain’s total transaction fee revenue, and consistently occupies three of Polygon’s top five gas-consuming contracts. The platform was valued at $9B in October 2025 following Intercontinental Exchange’s $2B investment.

The CLOB V2 upgrade Polymarket executed on April 28, migrating the exchange to a new collateral token (pUSD) and a rebuilt order book, runs on Polygon. That is a Polygon-native event and separate from the broader chain migration.

How the market priced it. That POL printed only +0.92% on a week stacked with Meta, Visa, and Modern Treasury integrations is the signal. The market is pricing both halves of the story rather than either alone: Polygon is adding the institutional payments rail at the moment it risks losing its largest crypto-native consumer application. The variable that determines whether POL re-rates higher or compresses from here is whether Polymarket’s migration timeline crystallizes into a confirmed exit or Polygon retains the platform through performance fixes. Stevens has committed to weekly engineering updates beginning in early May, which makes that timeline directly observable.

The bigger read for Polygon is that institutional distribution and crypto-native distribution are now competing inputs into the same fee base. Adding Meta, Visa, and Modern Treasury makes Polygon a payments rail; losing Polymarket would remove its largest crypto-native demand source. May’s question is whether the chain can keep being both at once.

3. Strategy adds another $255M, BTC Yield ticks to 9.6% YTD

Strategy disclosed on April 27 that it acquired 3,273 BTC for $255M during the week ending April 26 at an average $77,906 per coin. Total holdings stand at 818,334 BTC at a $61.81B cost basis (average $75,537 per coin), a position now slightly in profit at current prices. The week’s purchase was funded via 1,451,601 MSTR Class A shares sold under the at-the-market program. It marks the fourth consecutive week of buying, but at a meaningfully slower pace than the prior week’s $2.54B headline buy. MSTR shares closed near $172 on Monday after the disclosure, off the prior week’s high near $183, and finished the week at -4.07%.

mNAV sits at 1.28x, off the 2.4x peak from 2024 but well above the sub-1.0x readings that briefly forced an ATM pause in February. The capital structure has expanded beyond common-equity issuance: the company has $8.25B in outstanding convertible notes with strikes from $149.80 to $672.40 and a suite of preferred shares (STRC, STRD, STRK) issued through 2025. STRC’s volume-weighted average price of $99.76 in April held the dividend steady at 11.5% for a third consecutive month. The March $42B ATM filing across MSTR common, STRC, and STRK gives Strategy runway to keep accumulating through 2027 even at compressed premiums.

BTC Yield ticked from 9.5% to 9.6% YTD on the latest disclosure. Strategy has bought roughly 89,000 BTC year-to-date. The next disclosure is expected Monday May 4 for the week ending May 3.

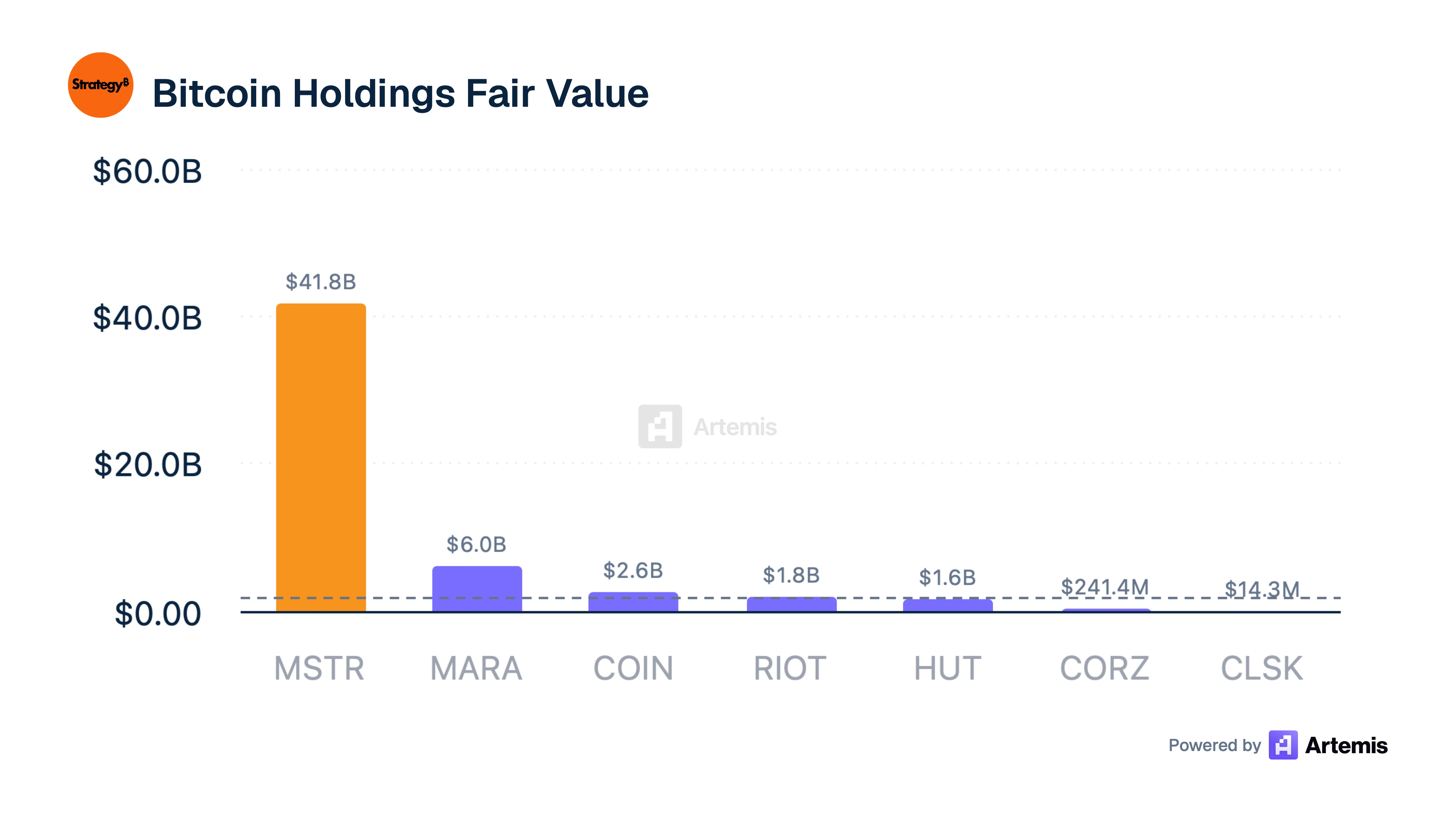

At $41.8B in Bitcoin fair value, Strategy holds nearly 7x the BTC position of the next-largest public corporate holder (MARA, $6.0B).

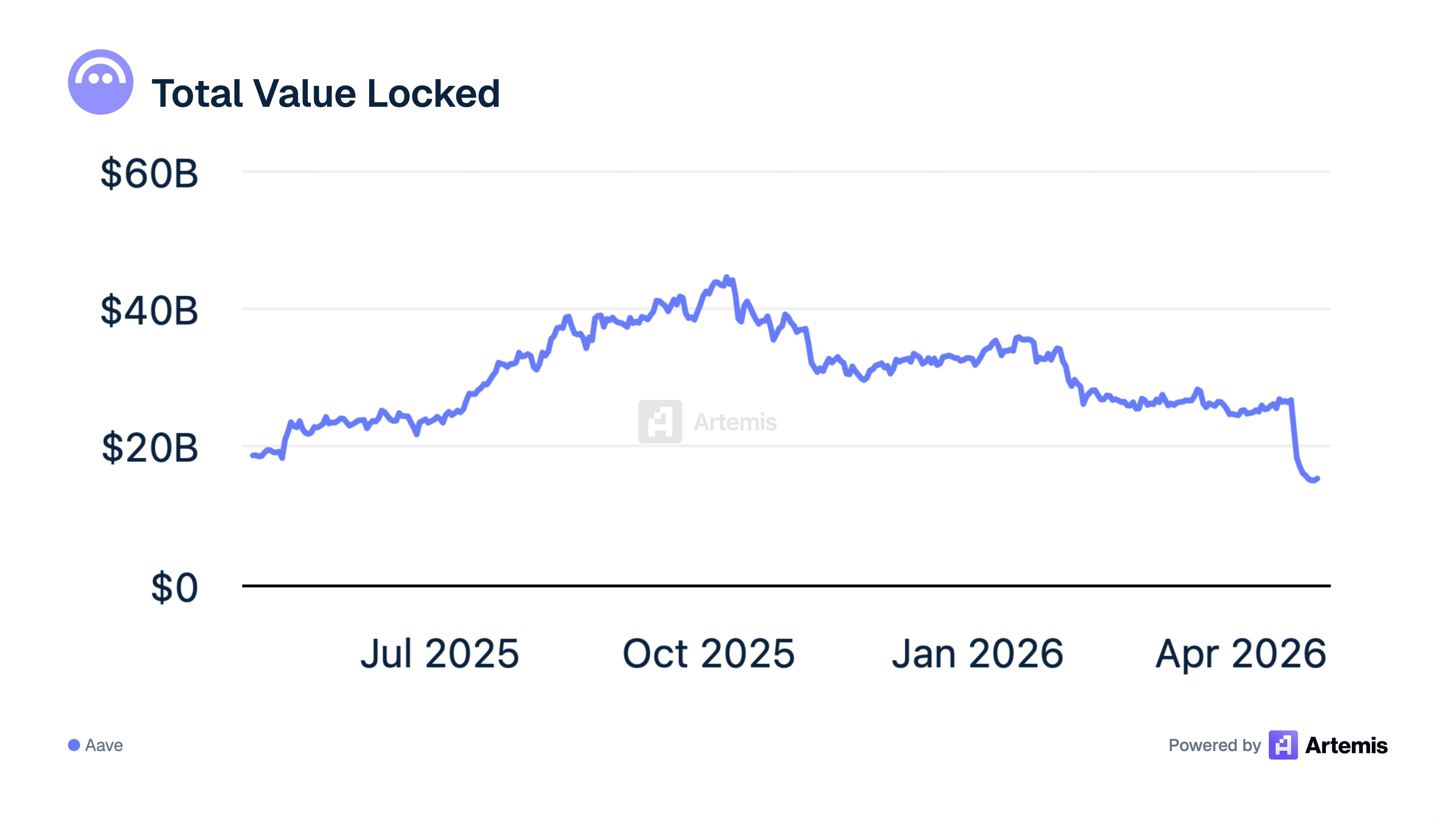

4. Aave coordinates the “DeFi United” bailout after KelpDAO contagion

KelpDAO’s rsETH cross-chain bridge was drained of approximately $293M on April 19, the largest DeFi hack of 2026. The attacker overwhelmed a security checkpoint with junk traffic and submitted fake transfer requests; the exploit was later attributed to North Korea’s Lazarus Group.

The contagion ran deeper than the exploit itself. Because rsETH was used as collateral on Aave, the attacker borrowed approximately 82,600 ETH (~$195M) against unbacked tokens, leaving Aave with bad debt despite its own contracts being uncompromised. Aave’s TVL fell from $26.4B to $20.1B over two days. Total DeFi withdrawals across the sector reached $13B. Two follow-on hits landed within days: Volo Protocol on Sui ($3.5M, April 22) and GiddyDefi ($1.3M, April 23).

By midweek, Aave service providers launched “DeFi United,” a coordinated recovery effort with Lido Finance, EtherFi, and Aave founder Stani Kulechov among those proposing to put forward ETH to cover the rsETH backing shortfall. AAVE held up better than peers across the basket at -1.55% on the week as the bailout took shape and the bad-debt overhang began to clear. Lido separately launched a $20M LDO buyback program funded from treasury stETH; LDO had rallied to 10-week highs the prior week before giving back -6.14% on the FOMC tape.

Charts of the Week

Other Notable News

Mastercard agreed to acquire BVNK Holdings, a London-based stablecoin infrastructure firm, for $1.5B plus up to $300M in contingent consideration, confirmed on the Q1 earnings call April 30. CEO Michael Miebach named stablecoins and agentic commerce as the two strategic pillars; Mastercard Agent Pay is in adoption by partners including OpenAI. Q1 net revenue grew 16% to $8.4B with adj EPS of $4.60 beating $4.41 consensus.

Visa reported fiscal Q2 results on April 28: net revenue of $11.2B grew 17%, the company’s strongest quarter in four years. Adj EPS of $3.31 beat the $3.10 consensus. The board authorized a new $20B multi-year buyback.

DOJ dropped its criminal investigation into the Federal Reserve and Powell late in the prior week, cited by Powell as a precondition for considering when to step down from the Board of Governors.

Wisconsin AG sued Kalshi, Coinbase, Polymarket, Robinhood, and Crypto.com over sports prediction market contracts. Separately, the DOJ filed what appears to be the first U.S. insider-trading prosecution tied to a prediction market: a Special Forces master sergeant who placed roughly $33,000 on Polymarket hours before Trump announced Maduro’s capture, netting more than $400,000. The Senate also unanimously banned members and staff from using prediction markets.

IBIT options open interest topped Deribit in late April, the first time U.S.-listed regulated BTC options have outpaced the dominant offshore venue.

Morgan Stanley launched MSNXX, a $1 NAV government money market fund built as a stablecoin reserves portfolio for issuers.

The Week Ahead

The data calendar quiets after the dense April 29-30 cluster. The April nonfarm payrolls report on May 2 is the next major macro print. ISM manufacturing and services bookend the week. On the crypto-adjacent earnings side, Coinbase reports Q1 after the close on May 7, the first read on subscription and services revenue inside the company’s $550-630M Q1 guide and the first meaningful disclosure of Base onchain revenue. Strategy’s next BTC purchase disclosure is expected Monday May 4 for the week ending May 3.

The macro question remains the same as last week: whether the Iran war’s oil pulse continues to feed PCE prints or whether near-term de-escalation cools the inflation impulse. The crypto question: whether ETF flows return to inflows after the three-day reversal into FOMC week, and whether $80,000 stops acting as resistance and starts acting as support.

Disclaimer: This newsletter is produced by Artemis for informational and educational purposes only. It does not constitute investment advice, a recommendation to buy or sell any security or digital asset, or an offer to provide advisory services. Artemis and its employees may hold positions in assets discussed. Figures are accurate to the best of our knowledge as of publication; markets move quickly.

Crushed it Akhil! Love the weekly man!