Why Robinhood is positioned to be the winner of retail finance

The bull case for HOOD as a financial super-app for modern generations NOT just a crypto correlated bet.

Summary: We believe that most investors view Robinhood (HOOD) as a cyclical retail brokerage that trades with Bitcoin. This narrow view misses that Robinhood is becoming a financial super-app for Gen Z and Millennials, the demographic we anticipate being on the receiving end of one of the largest intergenerational wealth transfers in U.S. history. Robinhood Gold is, in our view, poised to become the Amazon Prime of retail finance, turning subscription revenue into a flywheel that can make Robinhood higher quality, more recurring, and less cyclical over time. Prediction markets are an emerging new retail asset class — and Robinhood already has more than 20x the monthly active users of the next-largest distribution-native competitors like Polymarket and Kalshi. We believe asset per customers will keep growing due to Robinhood’s strong product velocity and foothold with Gen Z and Millennials, a demographic we expect to benefit from an impending intergenerational wealth transfer, positioning Robinhood as a winner of retail finance.

Intro

This memo is a joint perspective from Artemis and North Island Ventures (NIV). Artemis is a digital finance research firm focused on blockchain and equity assets. NIV is an NYC-based investment firm, focused at the intersection of blockchain, fintech, and AI.

Our shared view: Robinhood is misunderstood as a highly correlated bet on crypto and investors are missing that Robinhood is becoming a financial super-app benefiting from a generational wealth transfer and that HOOD should benefit from 2 catalysts in 2026: prediction markets and the mega-cap IPOs of SpaceX and potentially Anthropic and OpenAI.

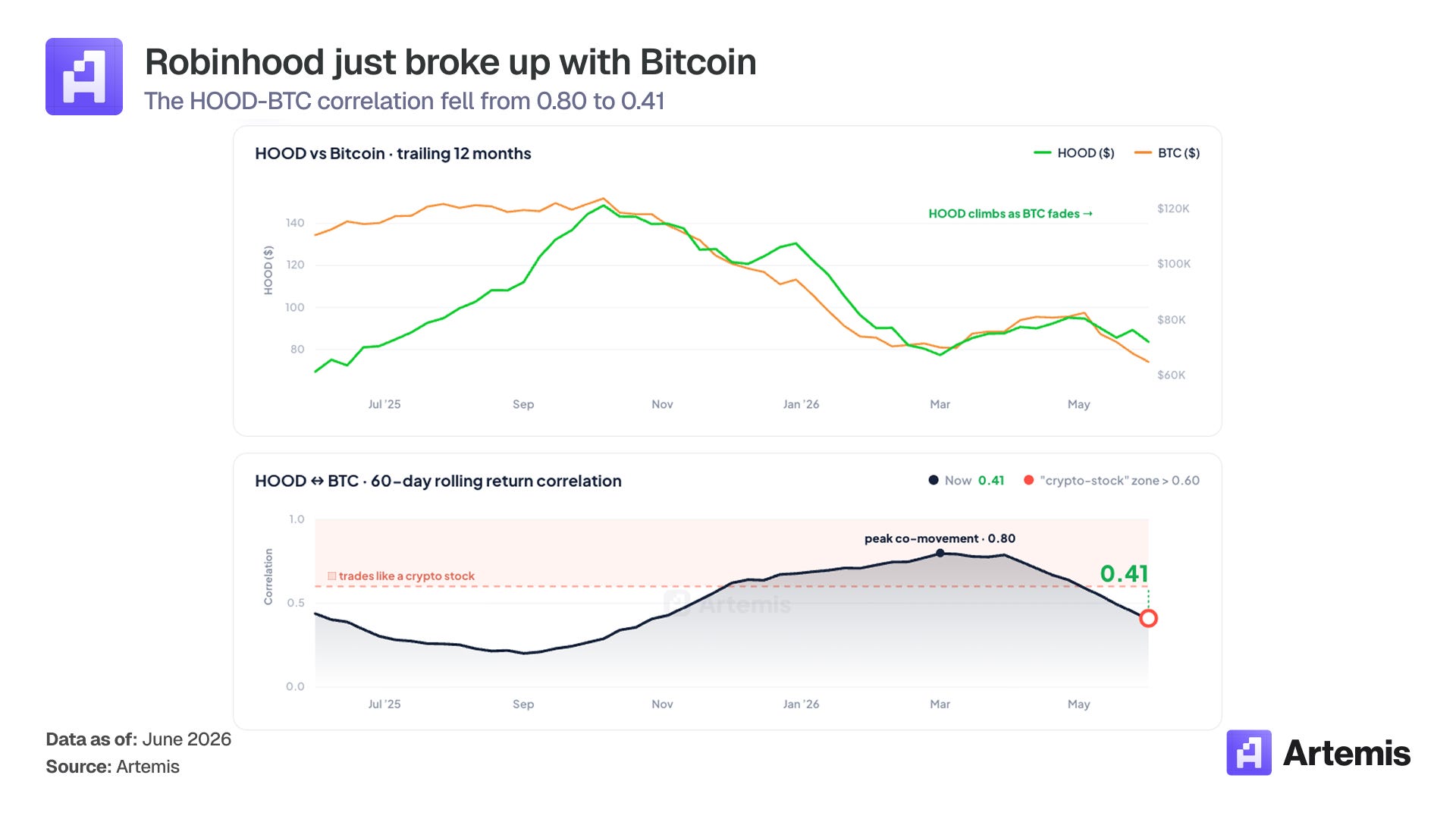

We believe that most investors still file Robinhood under “retail brokerage” and as an asset that heavily correlates with Bitcoin.

We want to demystify this assumption: Robinhood is finally becoming uncorrelated with Bitcoin with a correlation of 0.41 most recently after spending most of 2026 >0.70. The street prices the equity as if it is structurally tied to options and crypto trading cycles. We think that is wrong, and we think the mispricing closes as the super-app thesis becomes increasingly relevant.

1. The intergenerational wealth transfer and super-app. The median Robinhood customer is 35 years old, a demographic poised to benefit from Boomer populations’ wealth transfer to Gen Z and Millennials in the coming two decades, which we expect to be one of the largest intergenerational wealth transfers in U.S. history. While Boomer balances at legacy incumbents are more than 20x larger than Robinhood’s median customer’s average balance of roughly $12K, we view Robinhood’s relatively young customer base as positioning Robinhood to have little in terms of a legacy book to defend as compared to incumbents. The “why now” is the super-app. Robinhood finally has the product suite across investing, retirement, savings, spending, and speculating products to absorb the capital potentially coming from the intergenerational wealth transfer.

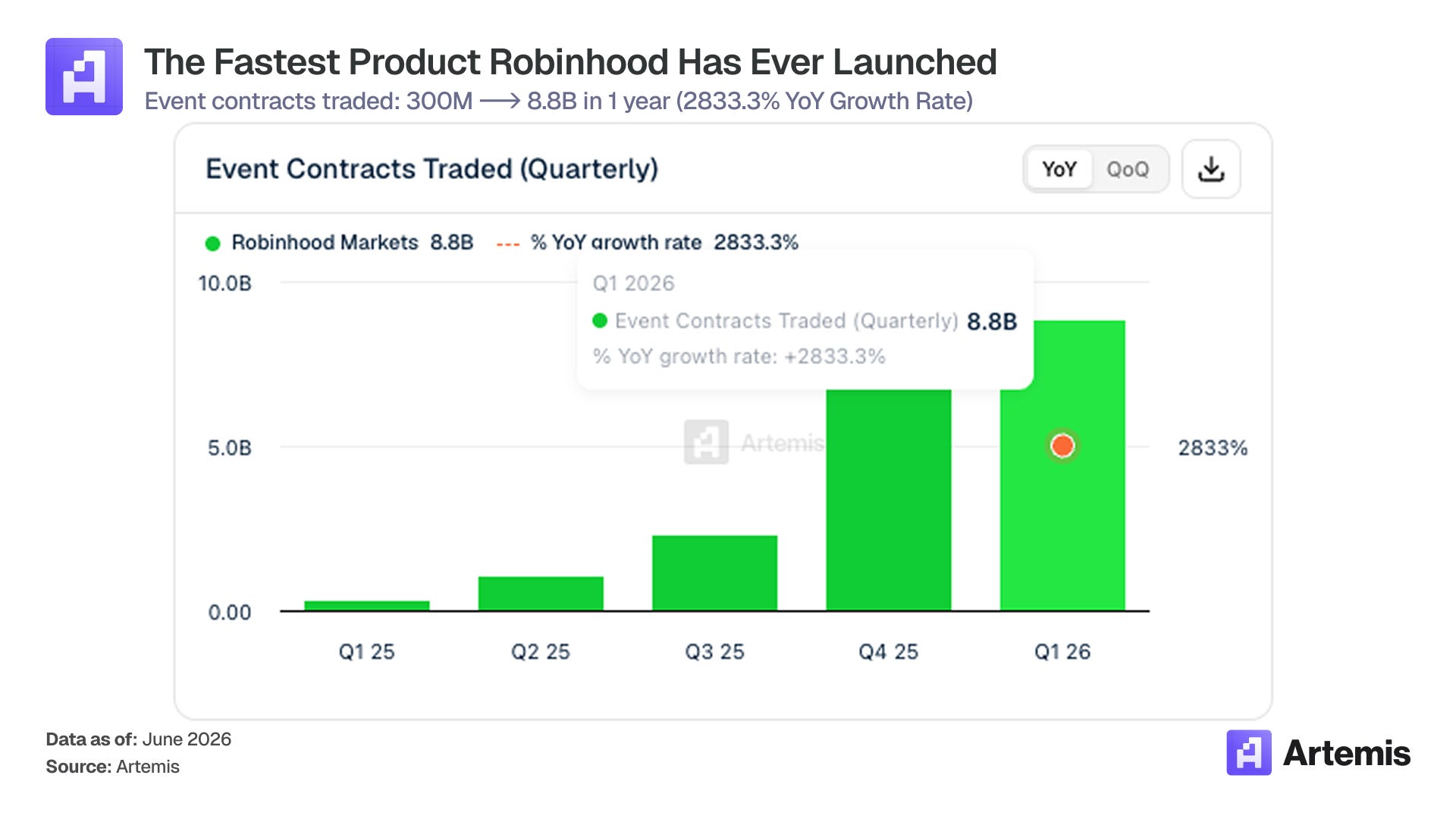

2. Prediction markets as a new retail asset class. Event contracts traded on Robinhood went from 300M in Q1’25 to 8.8B in Q1’26 — a 30× jump in four quarters. We estimate that prediction market revenue scaled from ~$3M to ~$104M over the same period. This is one of the fastest-growing product lines Robinhood has ever launched, with major catalysts still ahead: the World Cup, US mid-term elections, a full NFL season, and Rothera, Robinhood’s CFTC-regulated vertically integrated exchange and clearinghouse, going live.

We can already see a massive spike in prediction market volume on Kalshi and Polymarket that we expect will likely show up in Robinhood’s Q2 and Q3 ‘26 reported numbers as well.

Both tailwinds are early. Neither is reflected in the current forward multiple.

3. The mega IPOs could drive retail engagement. SpaceX is scheduled to IPO in early June and is planning to allocate a record 30% of shares to retail. Typical IPOs allocate 5-10% to retail. Anthropic and OpenAI may IPO in the coming months. The fundraising demand of these companies is unprecedented, and the retail interest appears strong. These IPOs could serve to increase engagement in Robinhood’s platform.

Why HOOD wins from the wealth transfer: Gold as the Amazon Prime flywheel

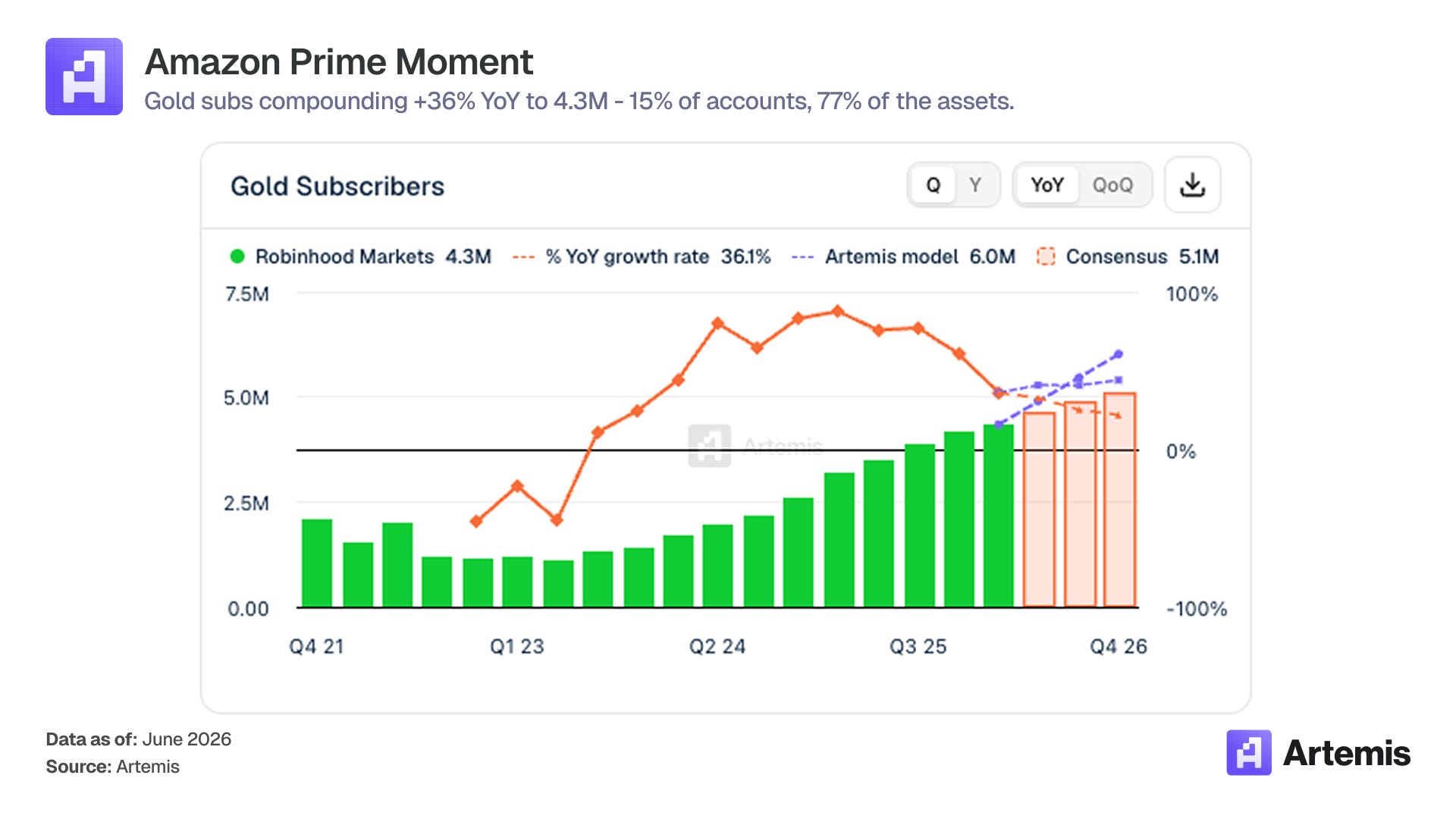

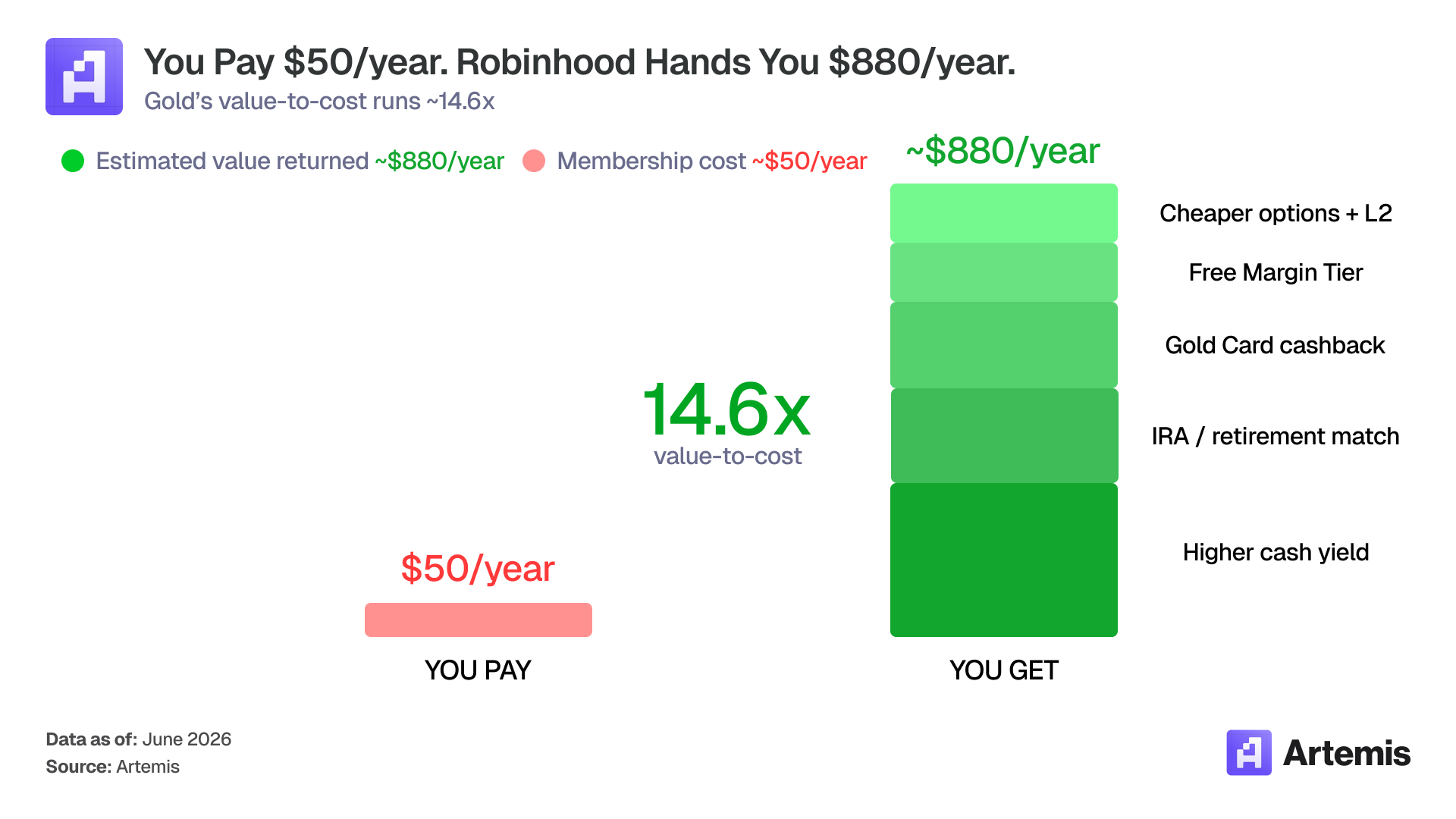

Gold subscribers grew from 1.14M at the end of 2022 to 4.34M in Q1’26 — 3.8× in roughly three years. The product costs $5/month (or $50/year). Our estimates put gross value to a member at ~$880/year (from higher cash yields, IRA match, free margin, cheaper options, Robinhood Gold Card, Morningstar research, Level II data, Robinhood Strategies).

What matters is the mix. Gold subscribers are ~16% of funded accounts but ~79% of assets on the platform. They are the asset compounders. Robinhood’s expanding product suite positions it well to convert more of their existing 27M funded accounts, into Gold subscribers. As Gold penetration rises, every metric that compounds — ARPU, net deposits, retention, gross margin — moves with it.

We believe Prime turned Amazon from a retailer into a consumer habit. The Prime subscription model increased engagement and ultimately spending on Amazon creating a stickier higher value customer. We believe Gold could do something similar for Robinhood and potentially make Robinhood the default financial home for the next generation.

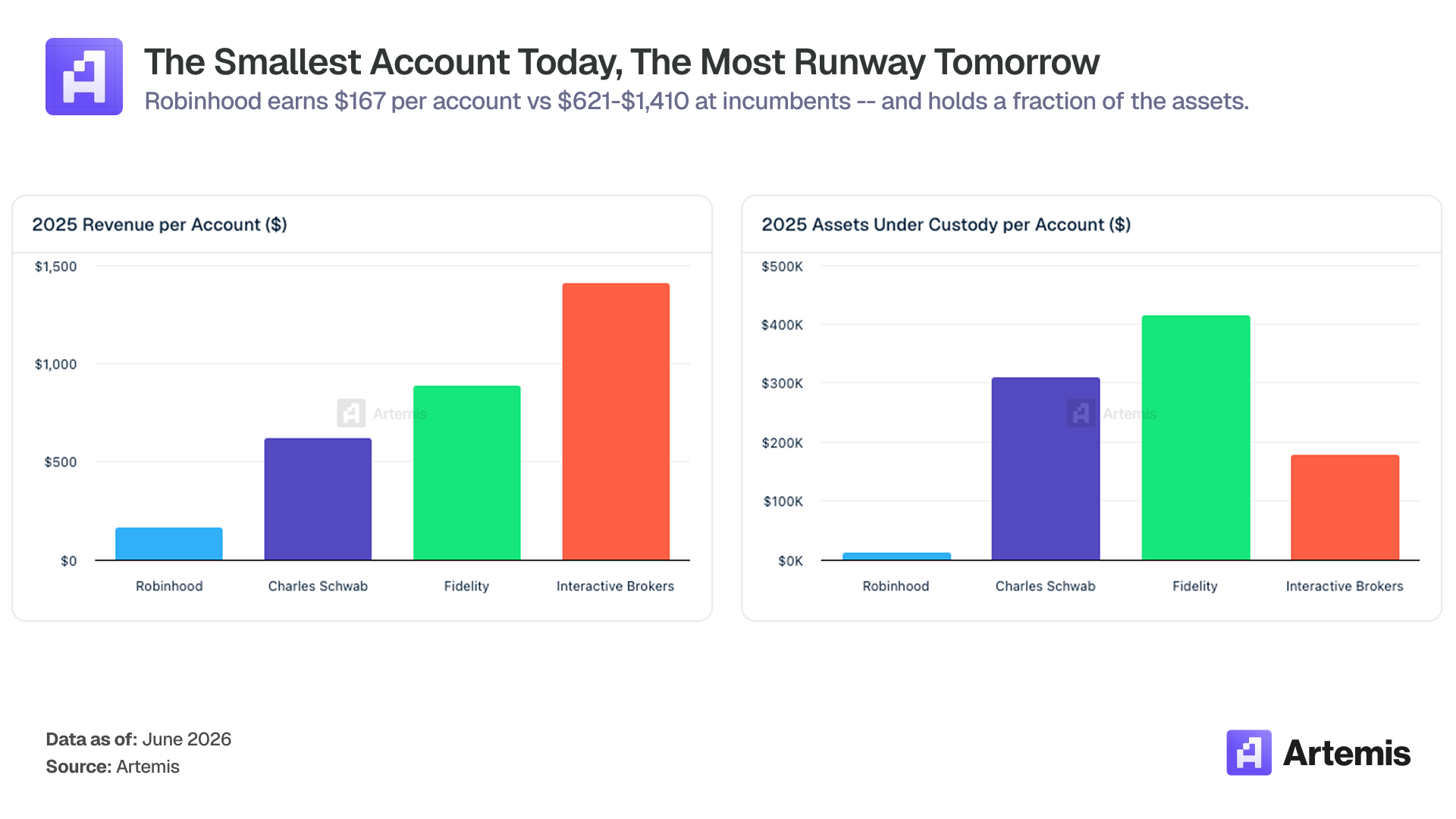

We believe that the asset base is converging. Average AUC per funded customer grew from $2,700 at the end of 2022 to $11,900 at the end of 2025. Even at that pace, HOOD assets per customer remain ~5% of Schwab, Fidelity, and Interactive Brokers — all of whom carry far older books.

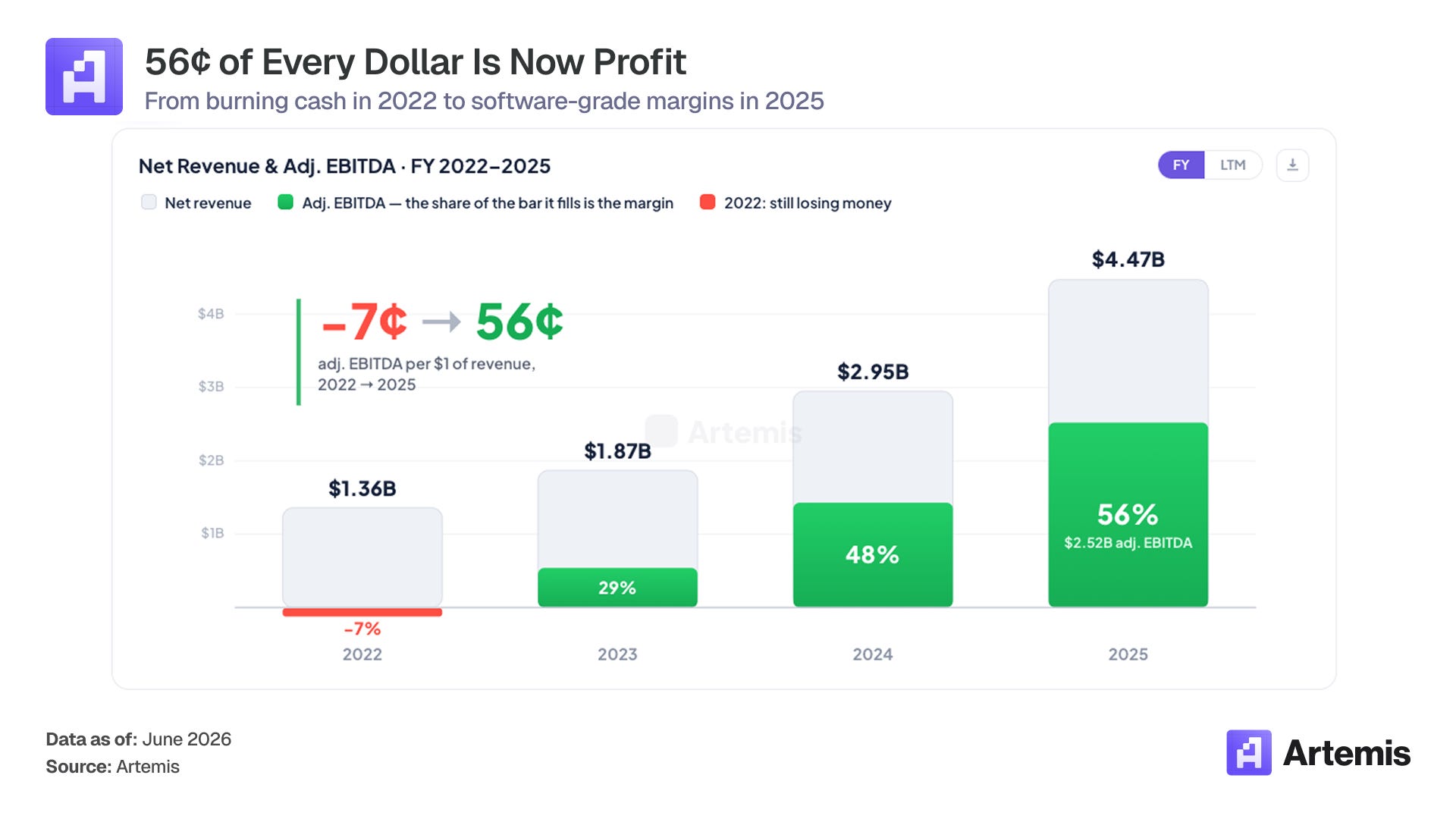

The margin profile shows the operating leverage has already arrived. Adjusted EBITDA margin went from -7% in 2022 to 29% in 2023, 48% in 2024, and 56% in 2025. Costs are largely fixed — technology, operations, and G&A together account for ~70% of the cost base — so incremental revenue lands at >70% incremental margins.

Why HOOD could win prediction markets

We believe this is the most underestimated part of the story.

In our view, three things make prediction markets a winner-take-most market: distribution, product UX, and integration with the user’s broader financial graph. We believe Robinhood could win on all three.

Distribution. 27M funded accounts and ~13M MAUs. Kalshi has an estimated ~5M MAUs; Polymarket has ~0.5M. The acquisition gap to the next-largest distribution-native competitor is more than 20×.

Product surface. Event contracts can sit alongside equities, options, and crypto in the same app, with the same wallet, statements, and risk system. Standalone prediction market apps cannot replicate that without becoming a brokerage.

Vertical integration. Rothera, the company’s CFTC-regulated exchange and clearinghouse, lets Robinhood control take rate, add markets quickly, and avoid paying a third-party exchange. Even at flat monetization, vertical integration typically expands contribution by 25–30%.

We treat prediction markets as a new asset class — like spot crypto in 2017 or zero-commission equity trading in 2014. The pattern we see in both prior cases: the broker that owns retail distribution captures the category and re-rates.

How HOOD monetizes the super-app

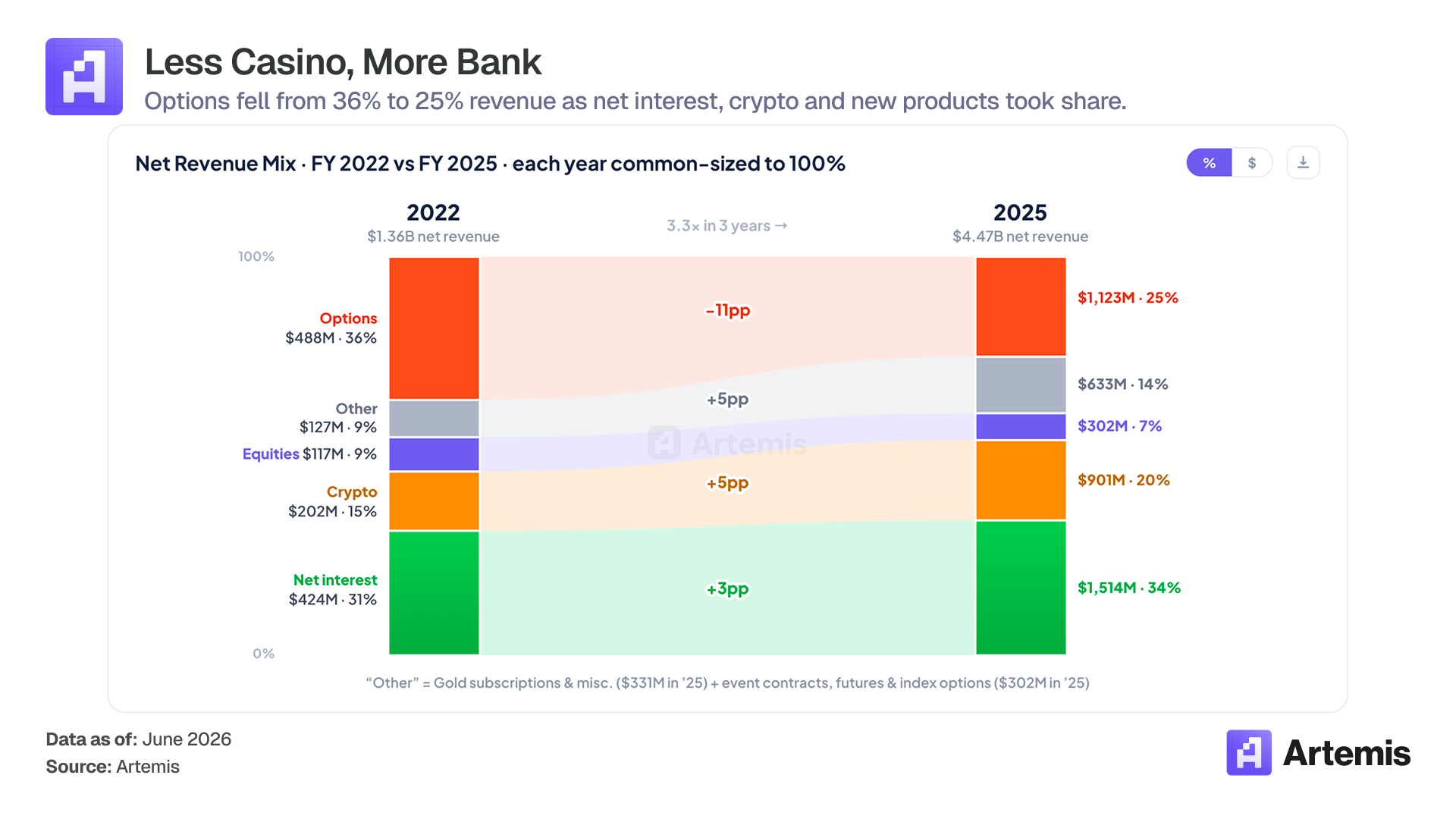

The shape of Robinhood’s revenue is changing.

The transaction line is no longer the whole business. Net interest, Gold subscription fees, prediction markets, Robinhood’s high-yield checking, the Gold Card, retirement (TradePMR added ~$40B in advisory AUM in 2025), Robinhood Strategies, and an early estate-planning push are all independent monetization lines. Each touches a different lifecycle moment and stickifies the relationship. Together, we believe they are converting Robinhood from a transaction-revenue business levered to speculation into a recurring-revenue platform whose customers monetize across their financial lives.

Why the market is mispricing this

HOOD trades at ~34x 2027 consensus EPS, which is roughly in line with Interactive Brokers and Coinbase. In our view, three things suggest HOOD is mispriced:

Gold mix is still ~16% of accounts. As it climbs, ARPU is structurally positioned to converge toward the $621–$1,410 range that incumbents earn per account, against HOOD’s $167 today. That is not a forecast — that is the structural setup of the business.

Prediction markets are already one of the fastest-scaling product lines in U.S. retail finance, and Robinhood owns the distribution.

The cost base is largely fixed. Adjusted EBITDA margin already hit 56% in 2025 with the platform still in investment mode.

Coverage hasn’t caught up because Robinhood is between buckets. Brokerage analysts under-cover it. Fintech analysts treat it as crypto-exposed. Crypto analysts treat it as a brokerage. That is exactly the kind of pricing gap where we expect the asset to re-rate after the fact, not before.

Conclusion

The market is viewing Robinhood as a cyclical retail brokerage. The business it is becoming — a vertically integrated financial super-app for the demographic poised to benefit from the intergenerational wealth transfer from Boomers to Gen Z and Millennials, with a fast-growing new asset class of the cycle running through its app — is, in our view, a different kind of company.

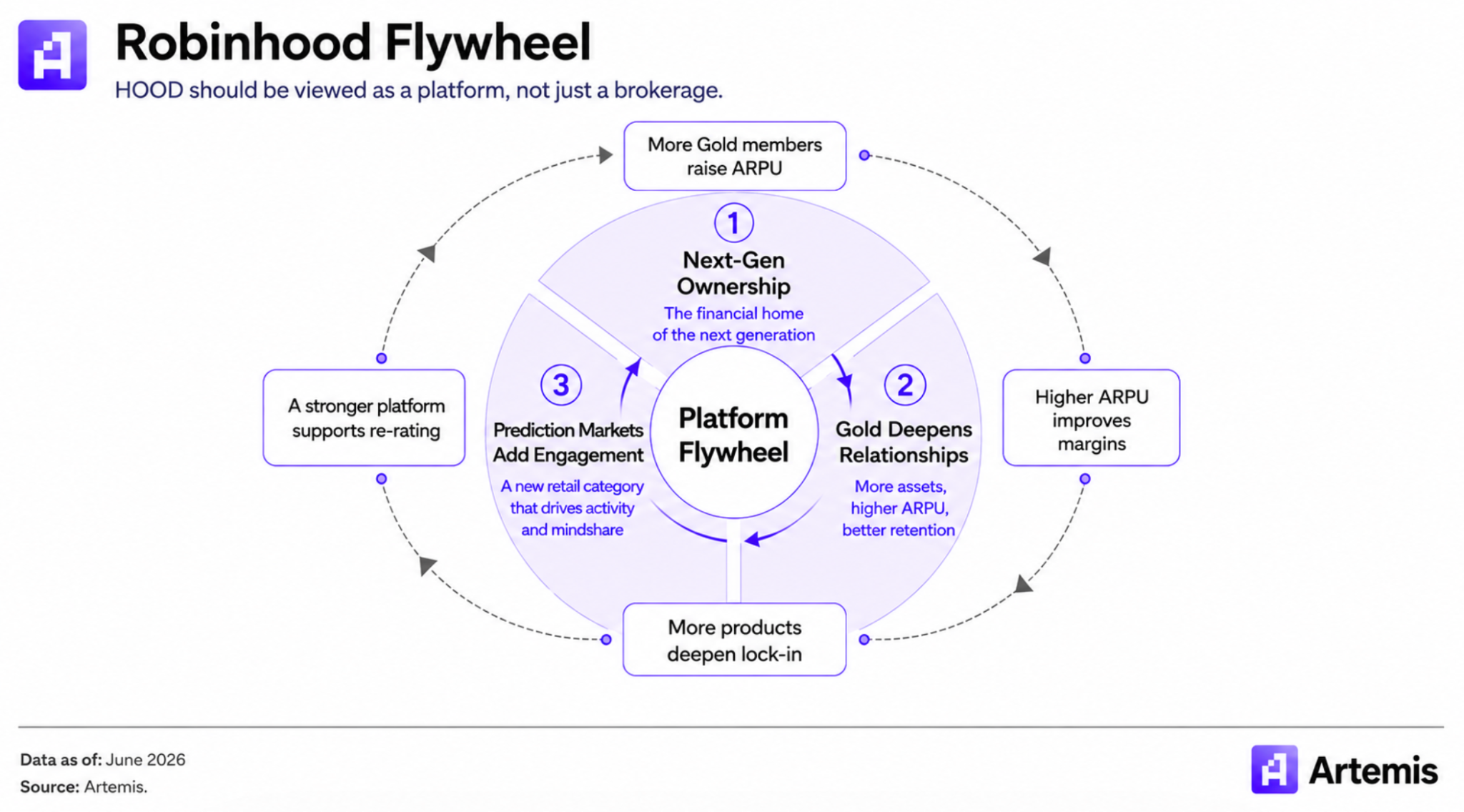

We believe HOOD should be benchmarked against the platform comp set, not the brokerage comp set. The flywheel of (1) demographic ownership × (2) Gold-driven asset compounding × (3) prediction market category leadership compounds. Each new Gold sub raises ARPU. Each ARPU dollar raises the margin. Each new product locks the customer in further. In our view, the longer this compounds, the more durable the franchise becomes.

We don’t think this is a 2026 story. We think this is the beginning of a decade-long platform shift in how the next generation saves, trades, borrows, bets, and builds wealth.

Important Disclosures

This article and all of the information presented herein is being provided by Artemis Analytics Inc. and North Island Ventures, LLC (“NIV”) (each an “Author” and together, the “Authors”) solely for informational purposes to provide educational content and general market commentary.

No statements included herein relate to or contain any offer of NIV’s investment advisory services, nor does any content herein, including but not limited to any referenced companies, constitute an offer to sell or the solicitation of any offer to buy any security or shares or interest in any of NIV’s current or future private investment funds (each a “Fund”), which may only be made at the time a qualified offeree receives the applicable confidential private placement memorandum, subscription documents and governing documents (collectively, the “Operative Documents”).

The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. NIV is not acting, and does not purport to be or act as, an adviser or fiduciary, in any capacity, with respect to any prospective investor in any Fund. A recipient of this article should consult his or her tax, legal, accounting or other advisors about the matters discussed herein.

While the information presented in this article is believed to be accurate, neither Author nor their respective affiliates or representatives (i) makes any express or implied warranty as to the completeness or accuracy of the information presented herein, (ii) shall be liable for errors appearing in this article or (iii) has any duty to update the information set forth herein. Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of terms such as “may”, “will”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, “continue“, “target” or “believe” (or the negatives thereof) or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or actual performance of investments may differ materially from those reflected or contemplated in such forward-looking statements. No representation or warranty is made as to such forward-looking statements.

Any analyses and opinions contained herein (including market commentary, statements or forecasts) may contain elements of subjectivity (including certain assumptions) or be based on incomplete or incorrect information. The Authors do not undertake to update the information contained herein.

This document displays certain trademarks and logos owned by the companies discussed herein. All such trademarks remain property of their respective owners, and are used only to directly identify or describe the companies being discussed herein. Their use is not intended to indicate and in no way indicates any sponsorship, endorsement or affiliation between the Authors or their affiliates, on the one hand, and the owners of such trademarks, on the other hand.

Accounts advised by NIV are currently invested in Robinhood and may make additional investments or exit positions at NIV’s discretion at any time for a variety of reasons and without further notice. No claim of performance (predecessor or otherwise) or prior track record is made in this document. Company metrics, including but not limited to, revenues, earnings, EBITDA, net income, and similar metrics, are not a proxy for the performance of a potential investment and should not be understood as such. There is no guarantee that achievement of any financial metrics, including changes in share price, will result in positive investment performance. Unforeseen or unaccounted for events could materially impact Robinhood’s performance and/or valuation—in such an event, projections could be materially altered. An investment’s performance is based on and must take into account a number of factors that the materials do not reflect, such as trading activity, terms of investment (e.g., share class), use of leverage, trading costs and other factors. Readers of this article should not interpret any presentation of share price as a proxy for any fund managed by NIV or investment performance. NIV makes no guarantee or assurance that any Fund will make similar investments. All investments are subject to the risk of total loss.

The discussions of Robinhood reference publicly-available information and certain estimates or projections have been provided by Robinhood or are primarily sourced from Robinhood. The Authors make no representation as to (i) the accuracy or reliability of any estimates or projections, (ii) the reasonableness of applicable assumptions and comprehensiveness of available inputs or (iii) the effectiveness or reliability of calculation methodologies. The Authors make no guarantee with respect to the prices at which any securities can be bought or sold. Numerous factors affect the performance of any investment.

| A guest post by

|